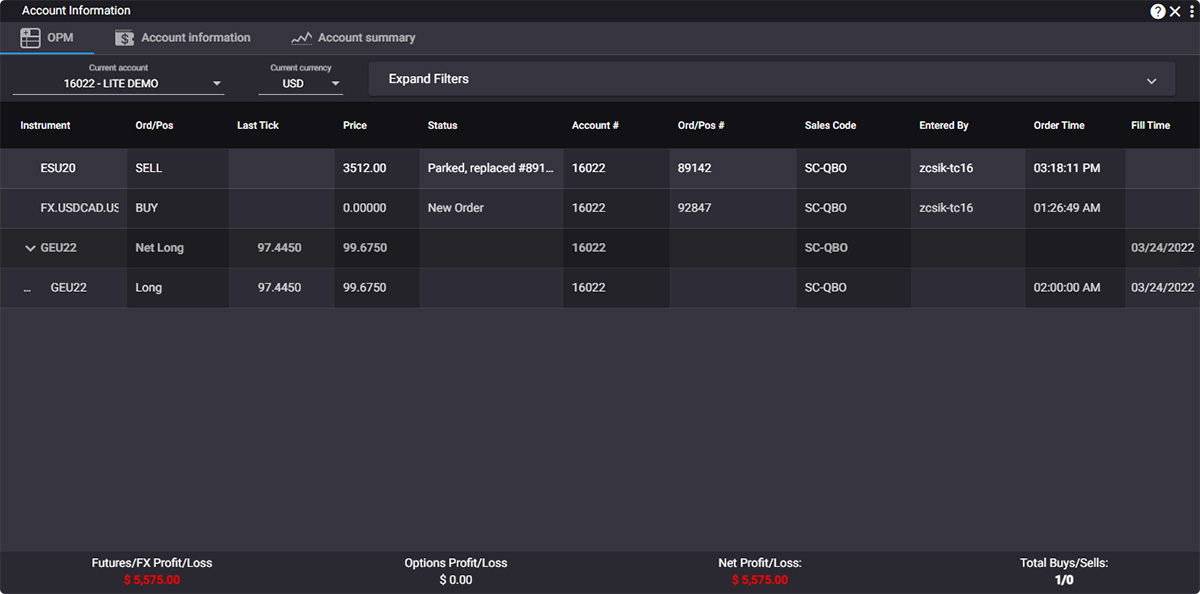

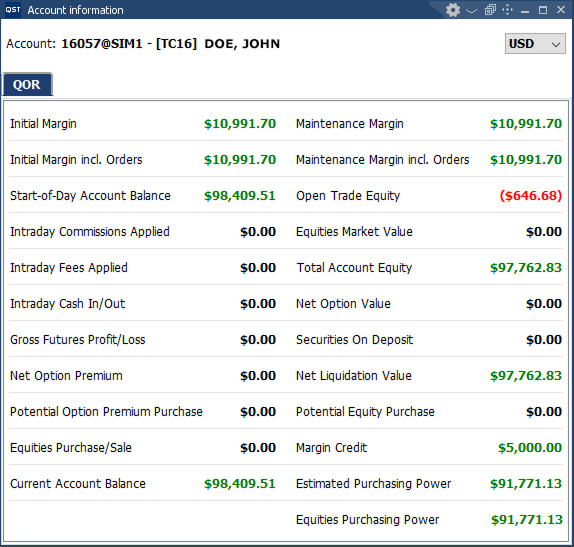

Account Information and Summary

Live Account Metrics

2/2

Orders & Positions

Filtering capabilities:

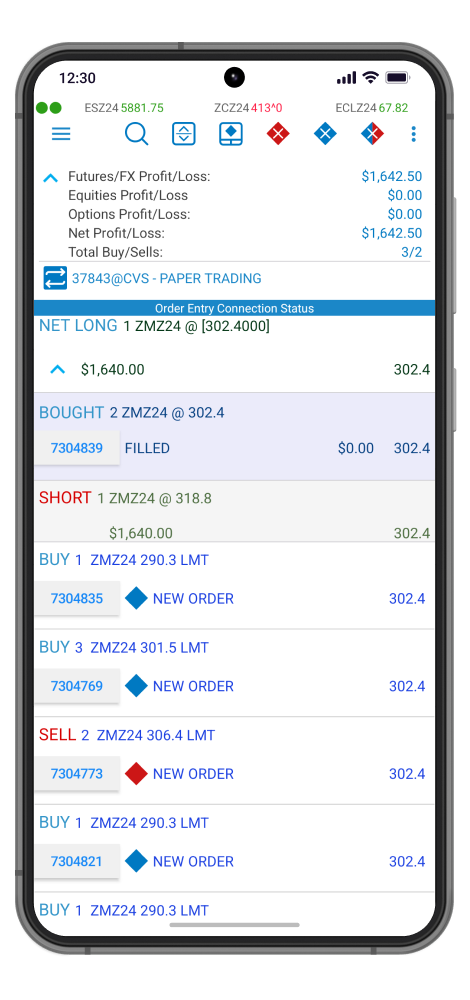

A dedicated status bar for Order Entry connection is displayed using color codes and explicit messages to inform about any network disruptions.

Important updates of your portfolio can be shown in Push-Notifications, In-App Notifications or Alert Dialogs. All these updates come together with a wide range of dedicated Order Entry Actions for a convenient and quick interaction.

3/3

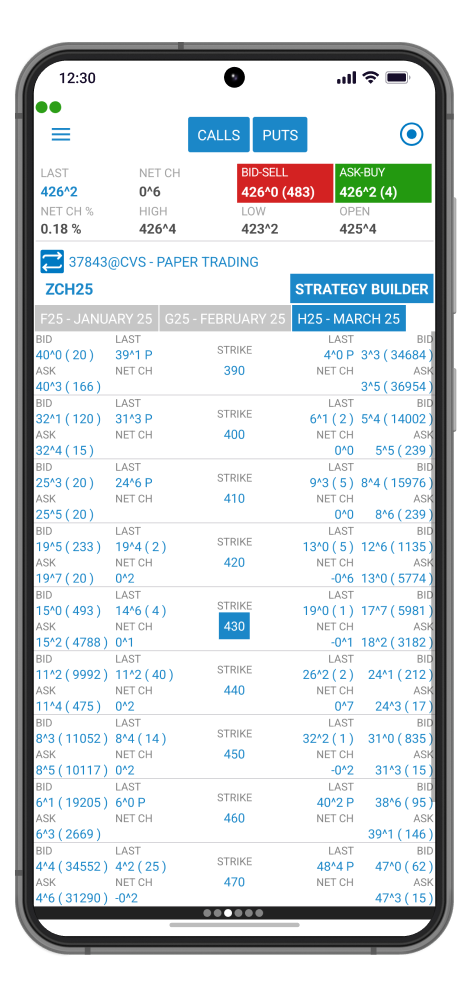

Options Chain

2/2

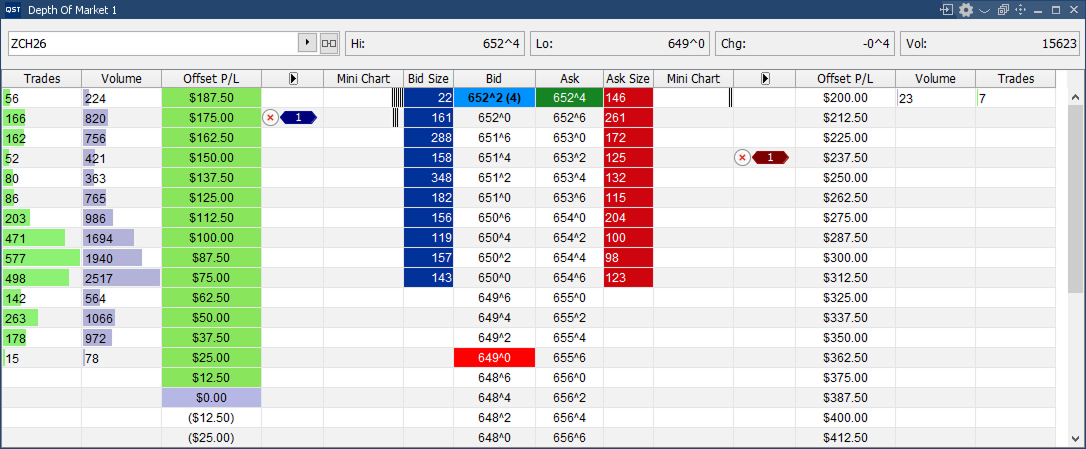

Depth Of Market

Order Entry Features

2/2

Price Ladder

Customization Features

2/3

Price Ladder

Order Entry Features

3/3

Order Entry/Management

2/2

Charts

4/4

Notifications

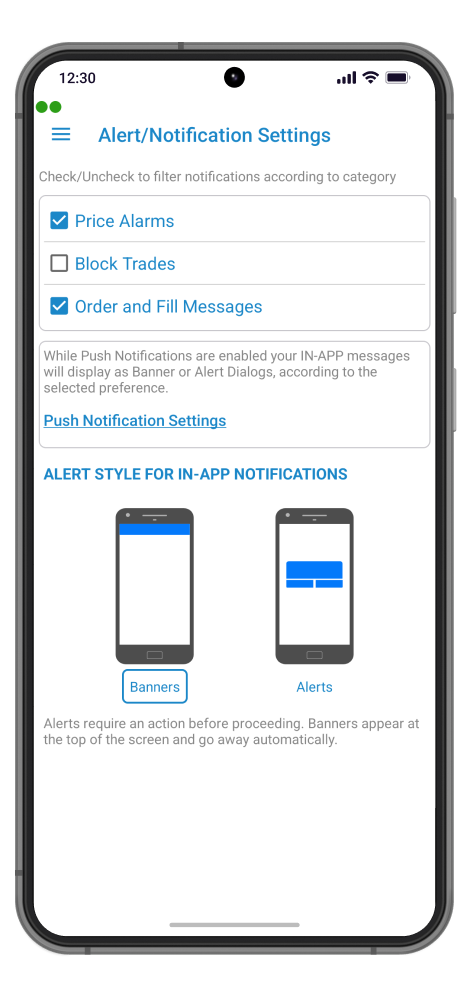

Push notifications while app is in the background can be easily activated for each defined category.

Two different ways to visualize your in-app notifications as banners or dialogs.

Specific categories of notifications for: Block Trades; Price Alarms; Order Entry.

Useful short description dedicated notification actions according to category; Enable/Disable for Block Trades and Price Alarms; Place Order, Cancel, Cancel/Replace, Offset, Reverse for Order Entry Notifications.

2/2

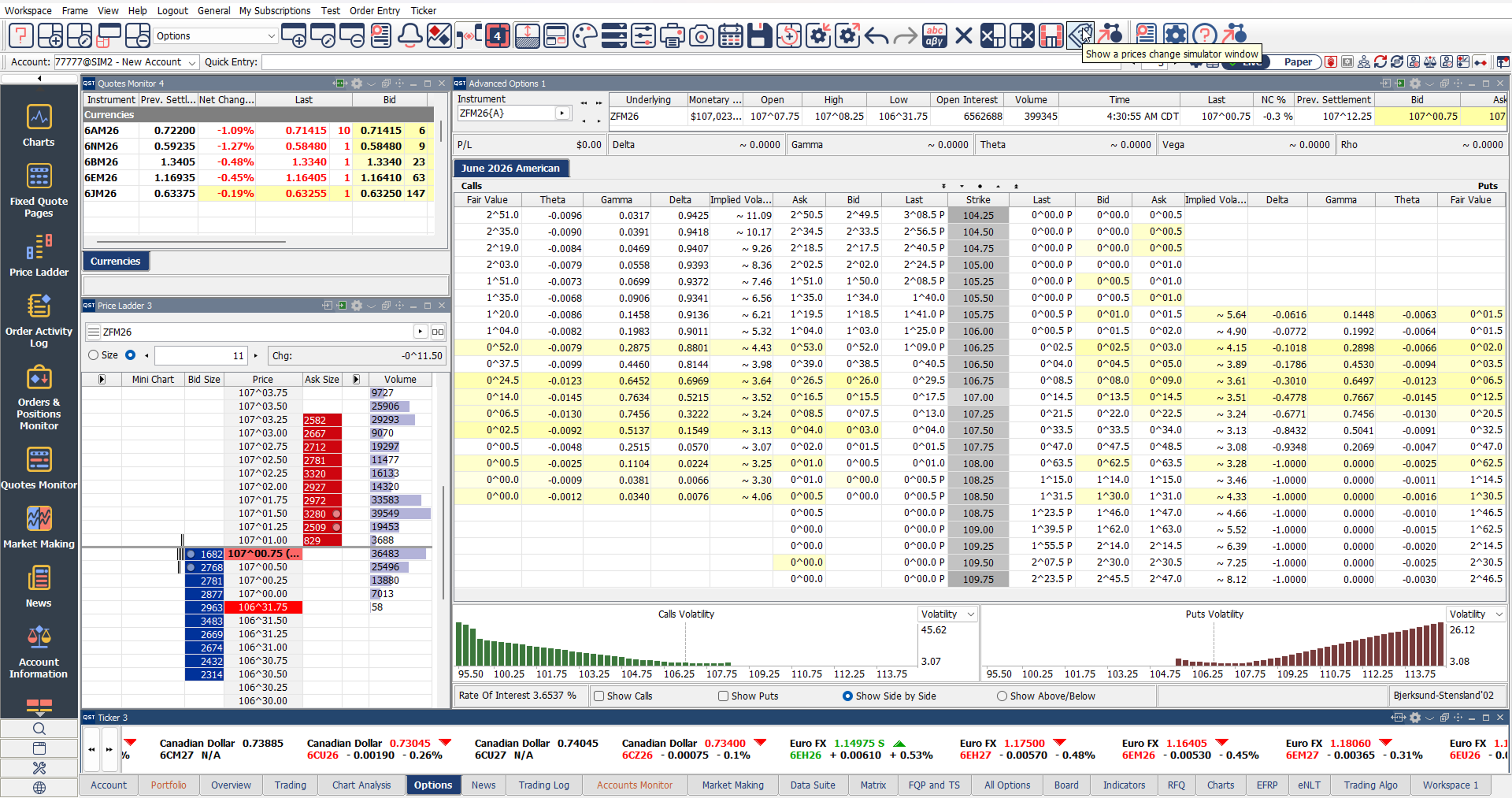

Advanced Options

1/2

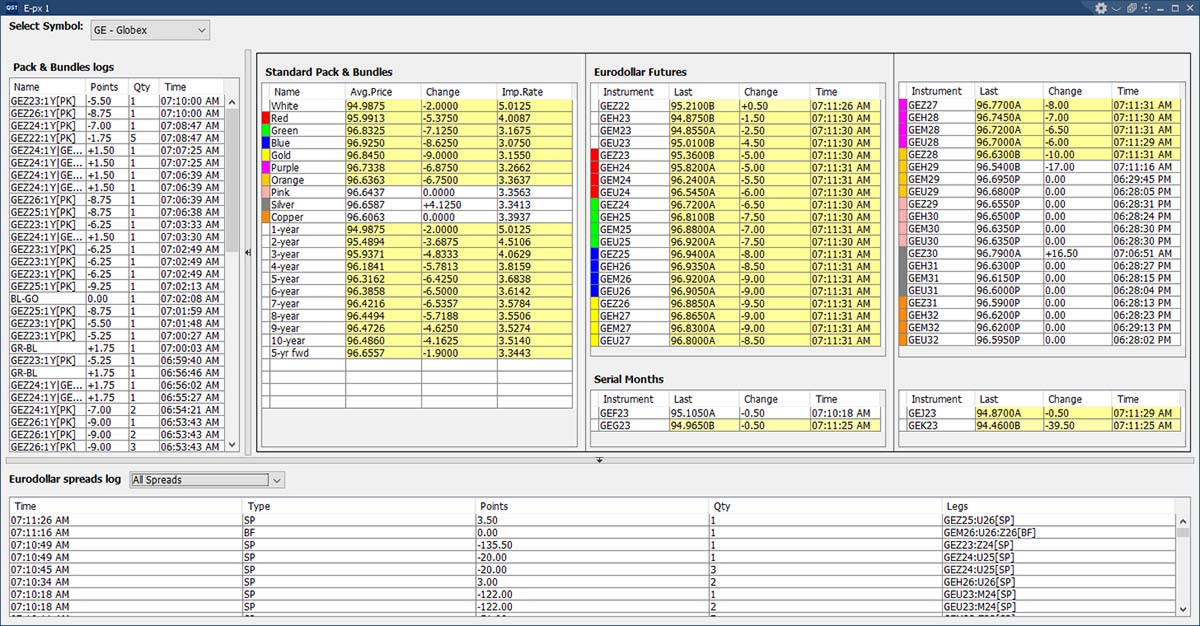

Quotes Monitor

2/2

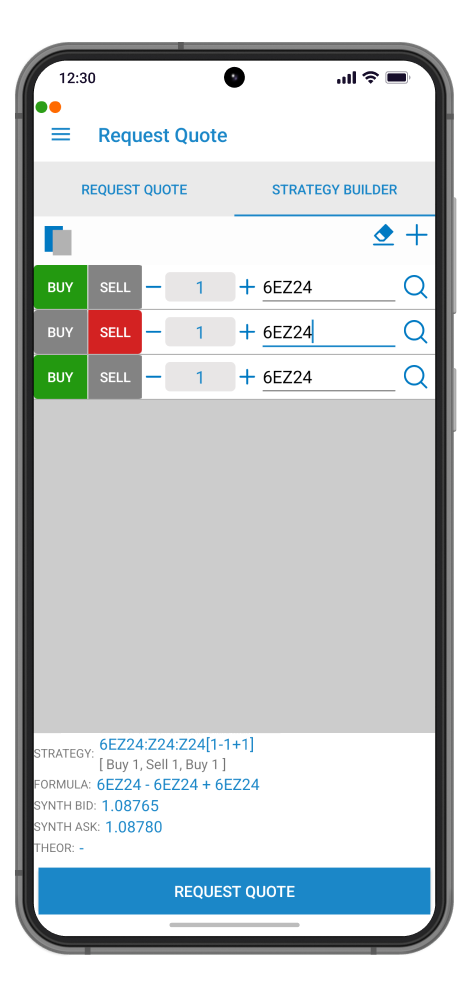

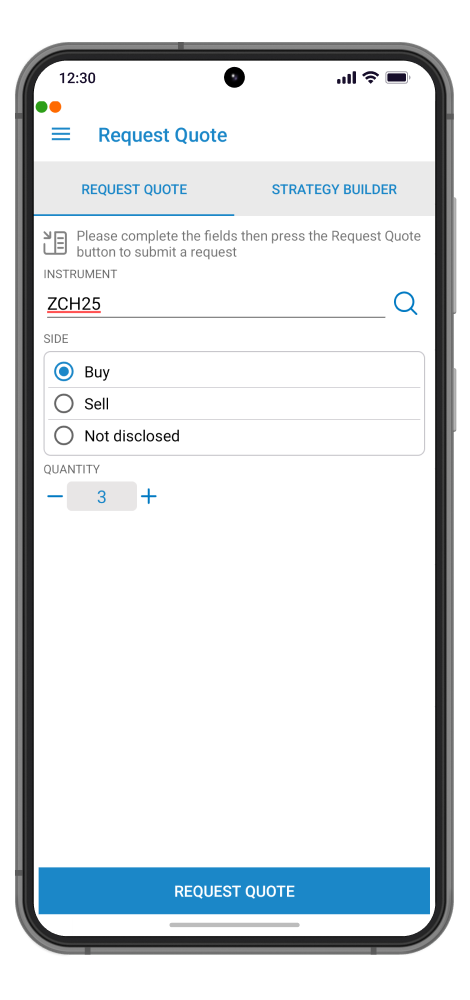

Strategy Builder

Strategy Builder, starting from a quote or from Options Chain module, you can build your own strategy quickly and easily.

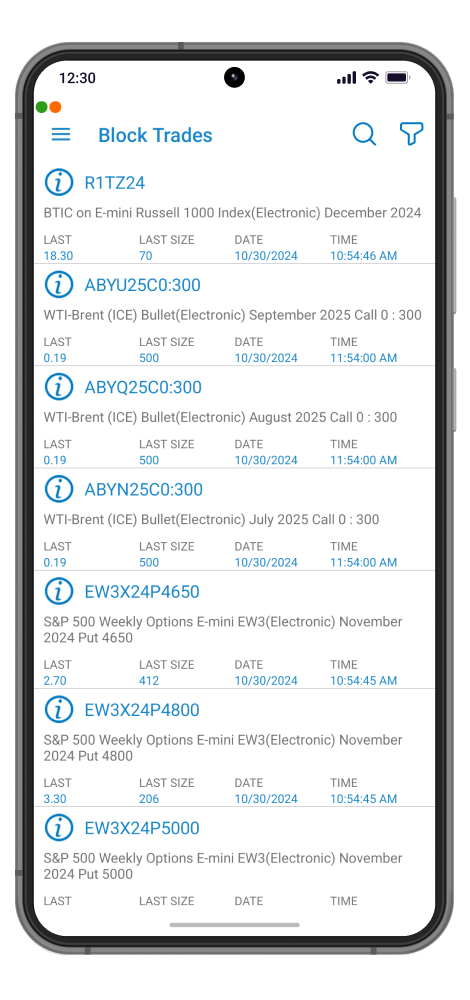

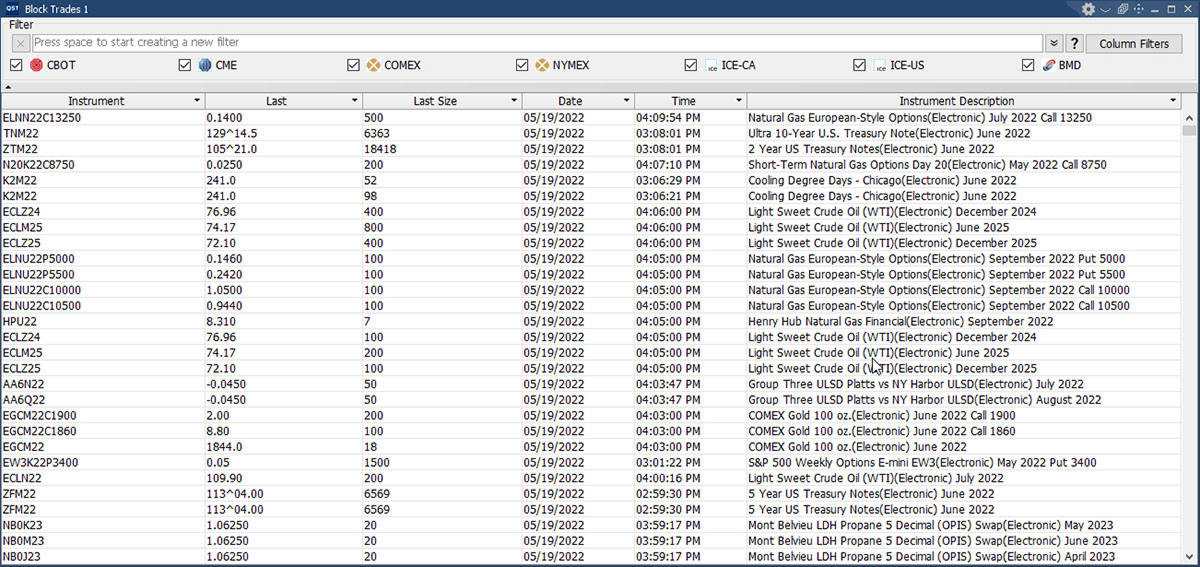

Block Trades

Block Trades provides you with a real-time blotter of block trades.

Notifications

Allows users to enable or disable available alerts and notifications(push notifications & in-app notifications).

A filter for notifications is available according to category, as follows:

1/2

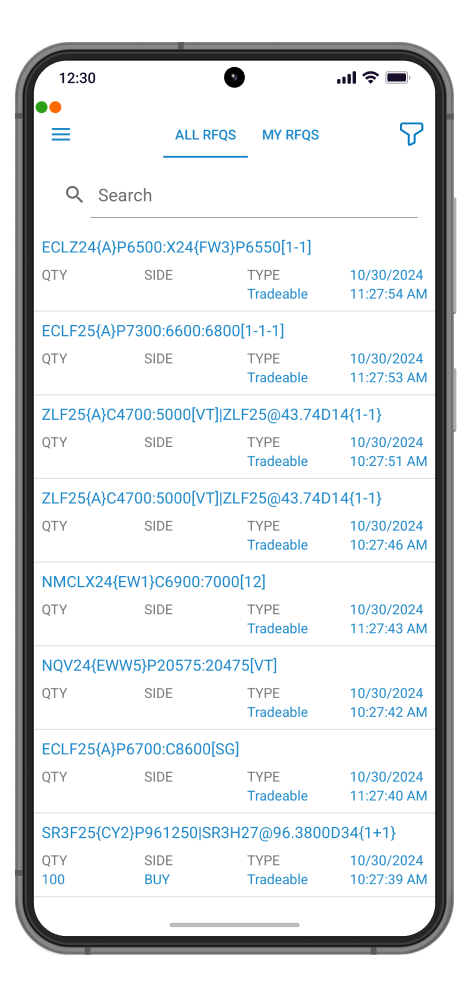

Show RFQ

Show RFQ, a real time updating module showing both your RFQ and all the available RFQs sent by other traders.

Quick filter are offered to show either “All” or “My RFQ”.

Extra filters are for:

A dedicated search bar for quick search is readily available on screen.

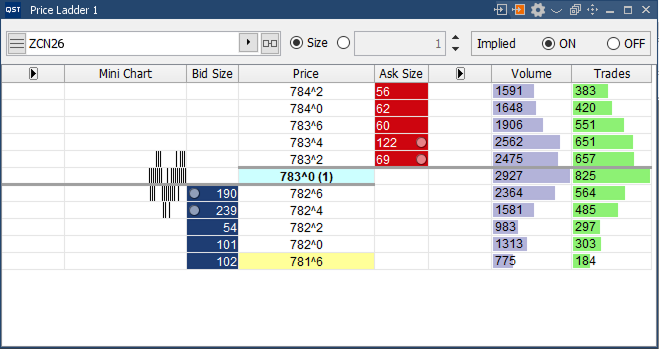

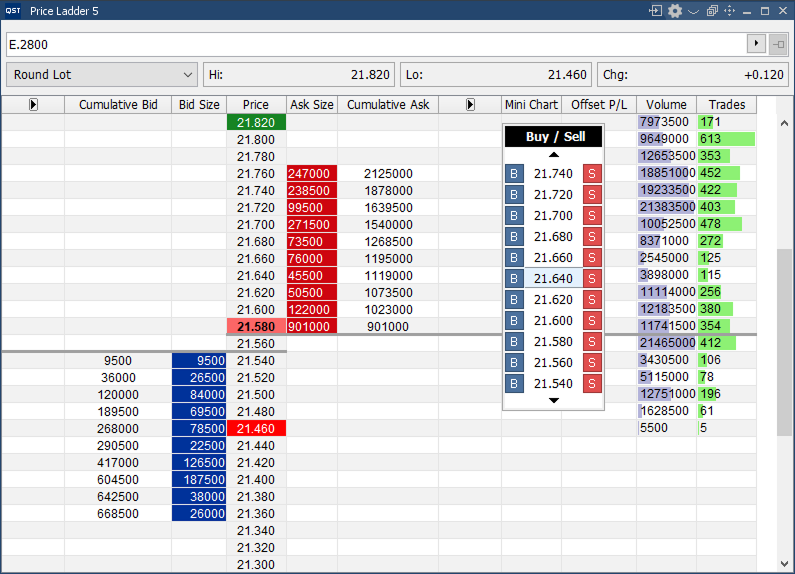

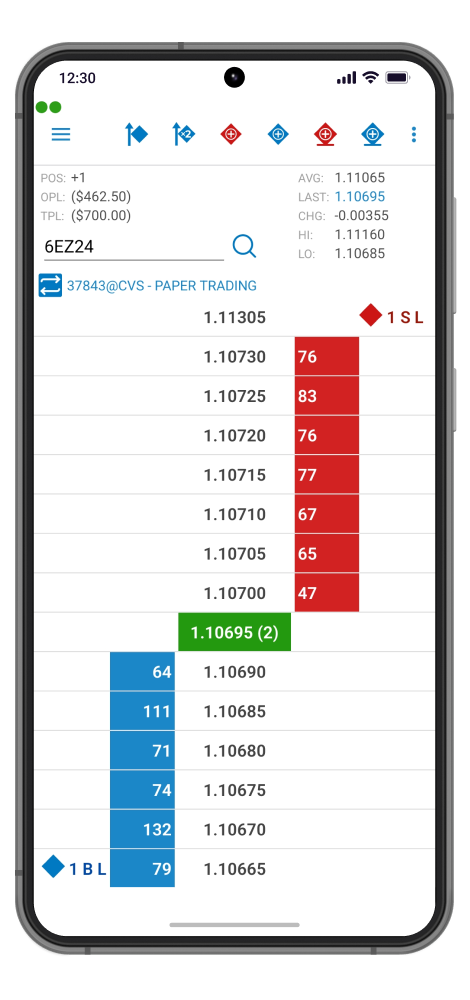

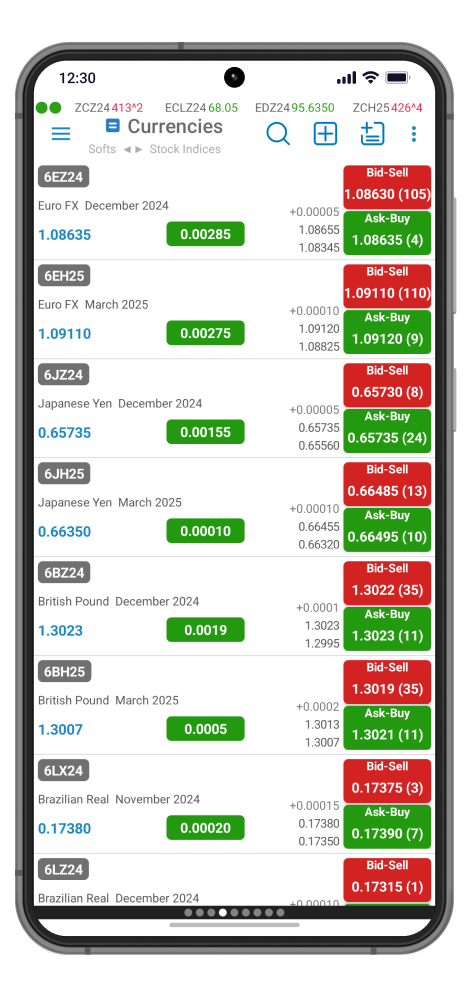

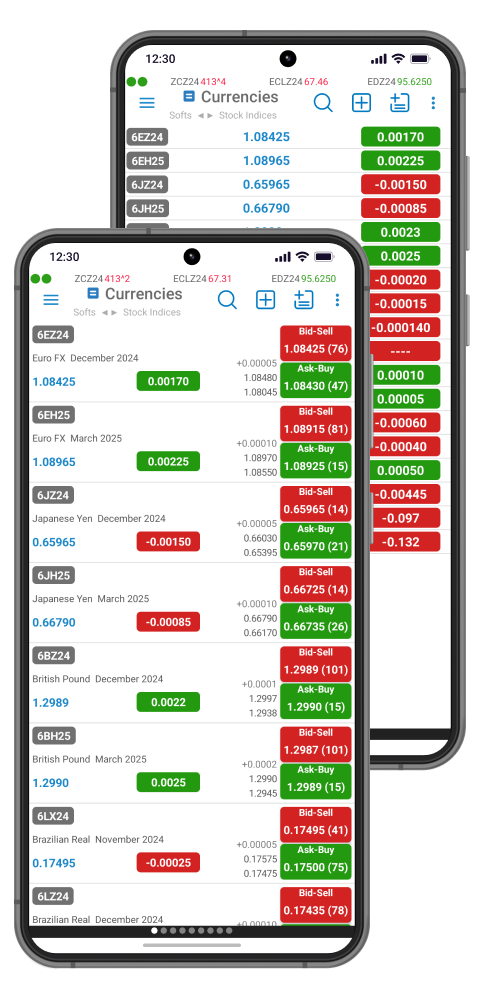

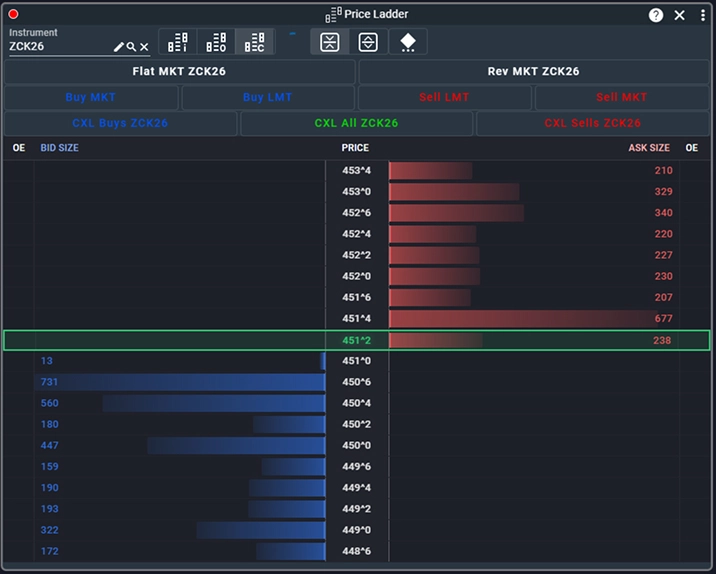

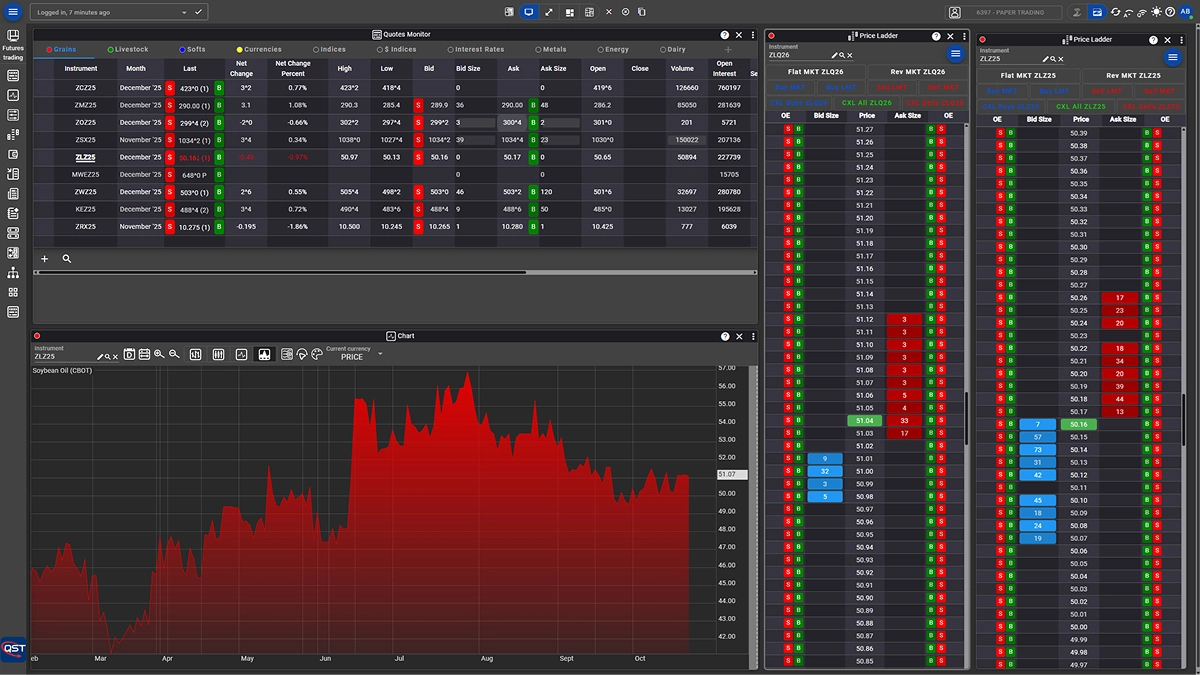

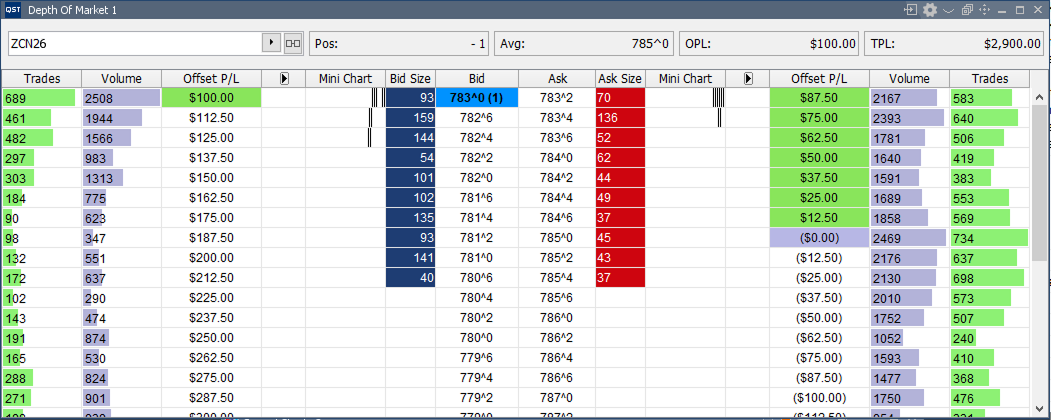

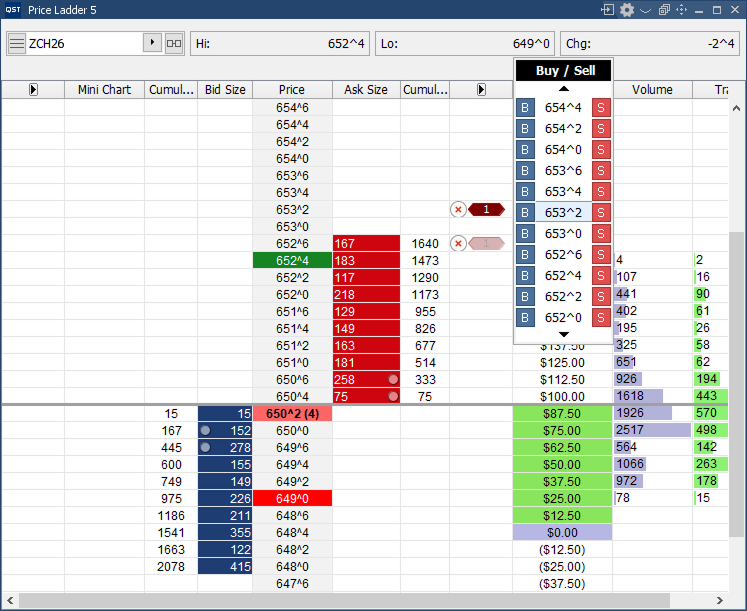

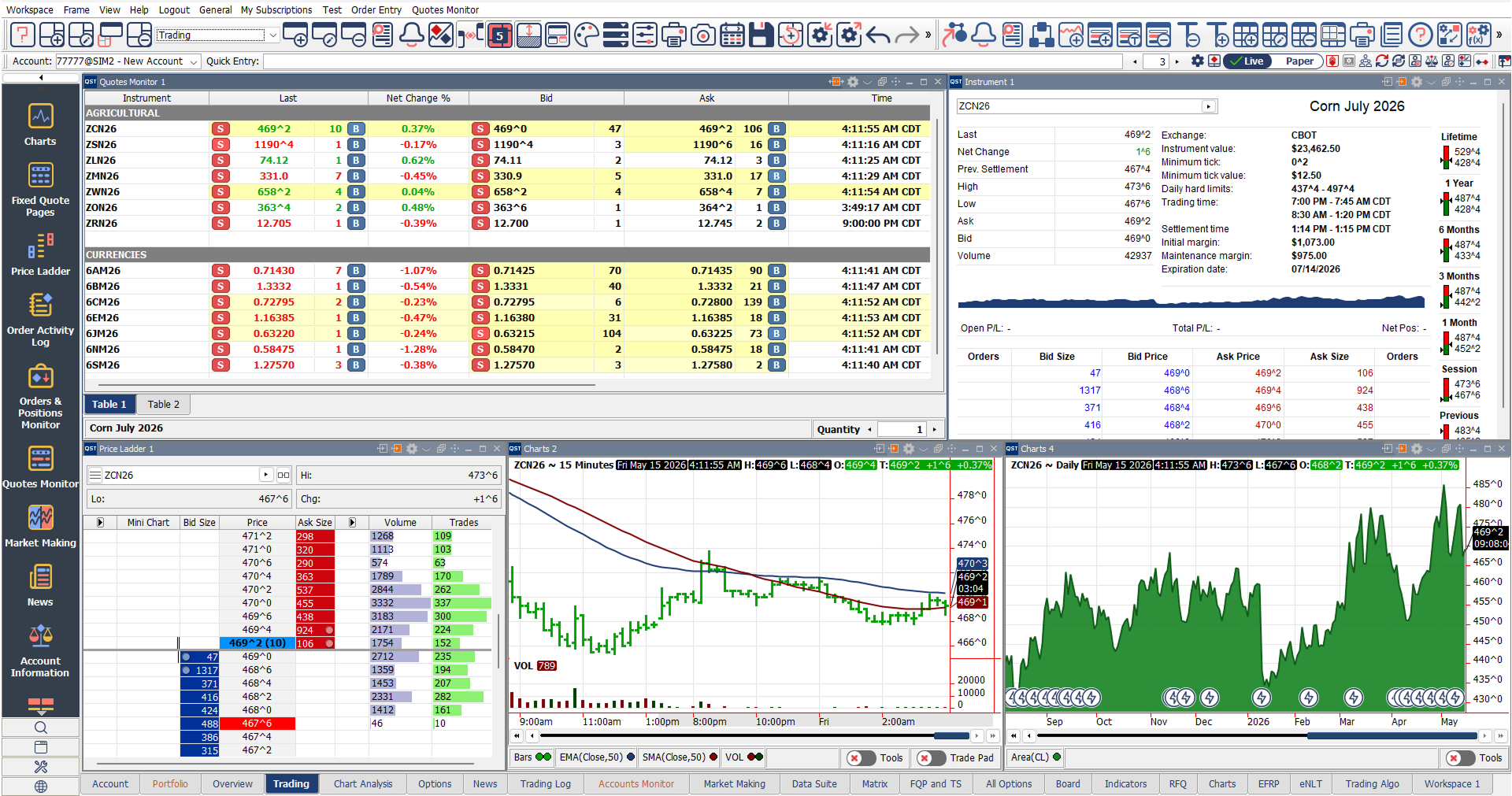

Price Ladder

Price Ladder offers a real-time market depth view utilizing a vertical layout that also shows your orders and positions.

Displays detailed information about a given instrument.

Shows the total number of:

Displays bid and ask size.

The Left and right margins of the ladder represent the buy and sell Order Entry columns.

Allows users to Place, Cancel and Cancel/Replace orders with simple gestures such as double tap or drag and drop.

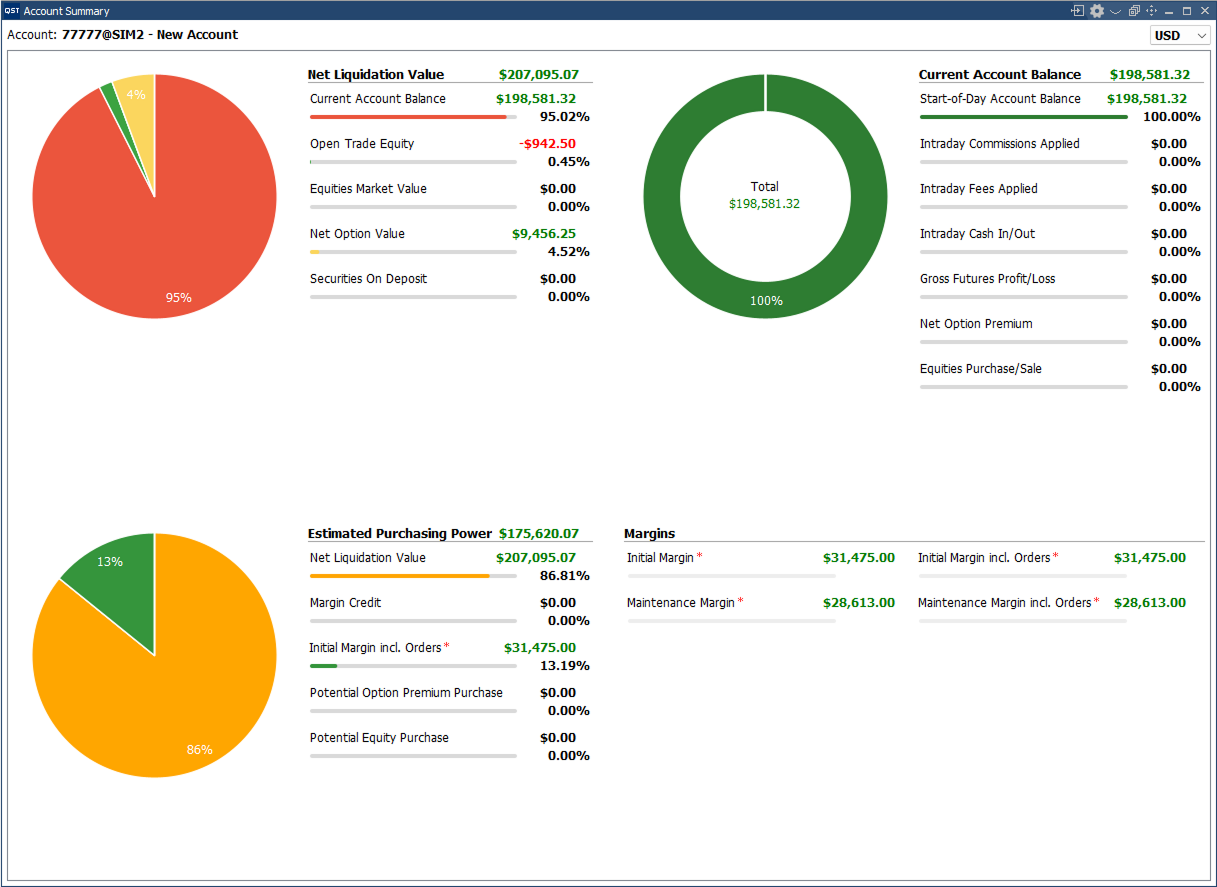

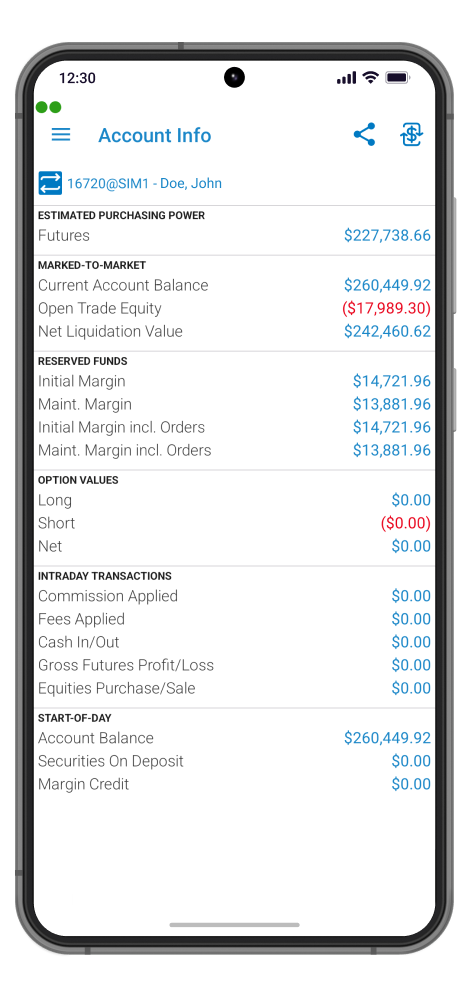

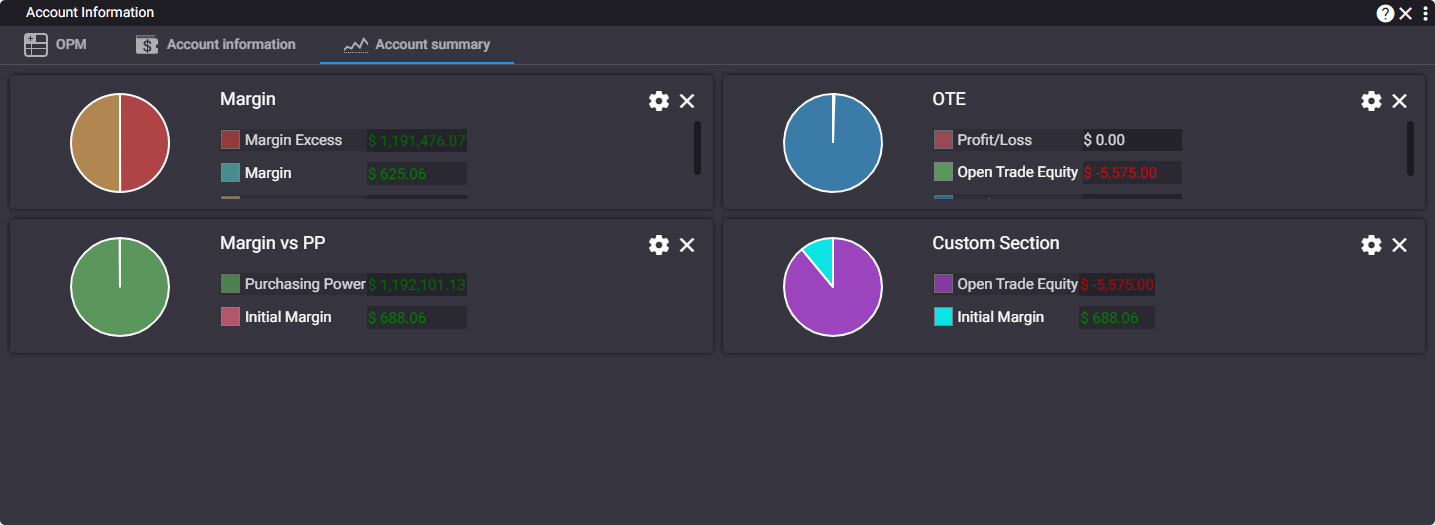

Account Information

Recalculated in real-time with each new tick or fill:

Real-time account calculations including:

Quick export button is available on screen in order to save data in a pdf file.

Currency can be easily change and all data on screen will update to the new currency instantly.

Switch account is available for a fast switch between several accounts.

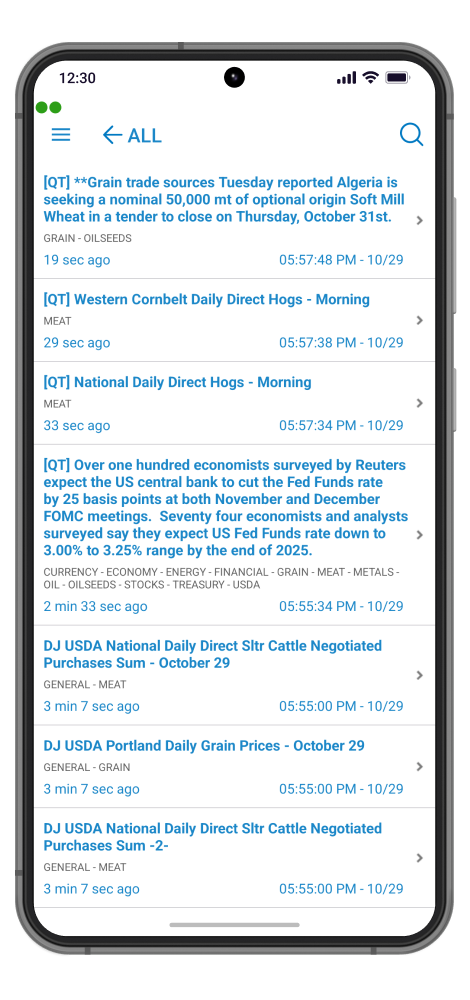

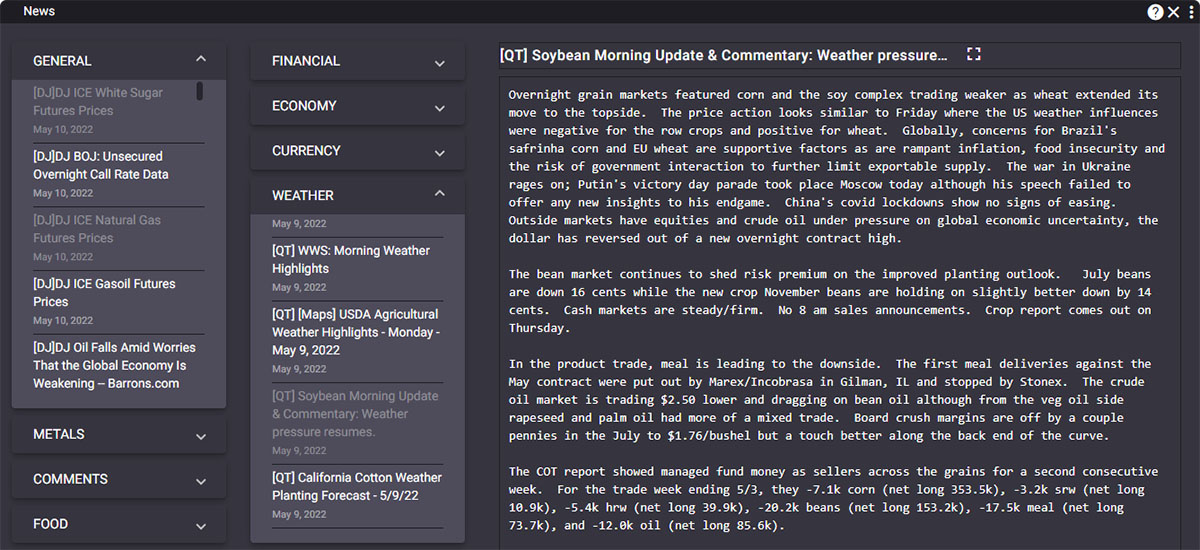

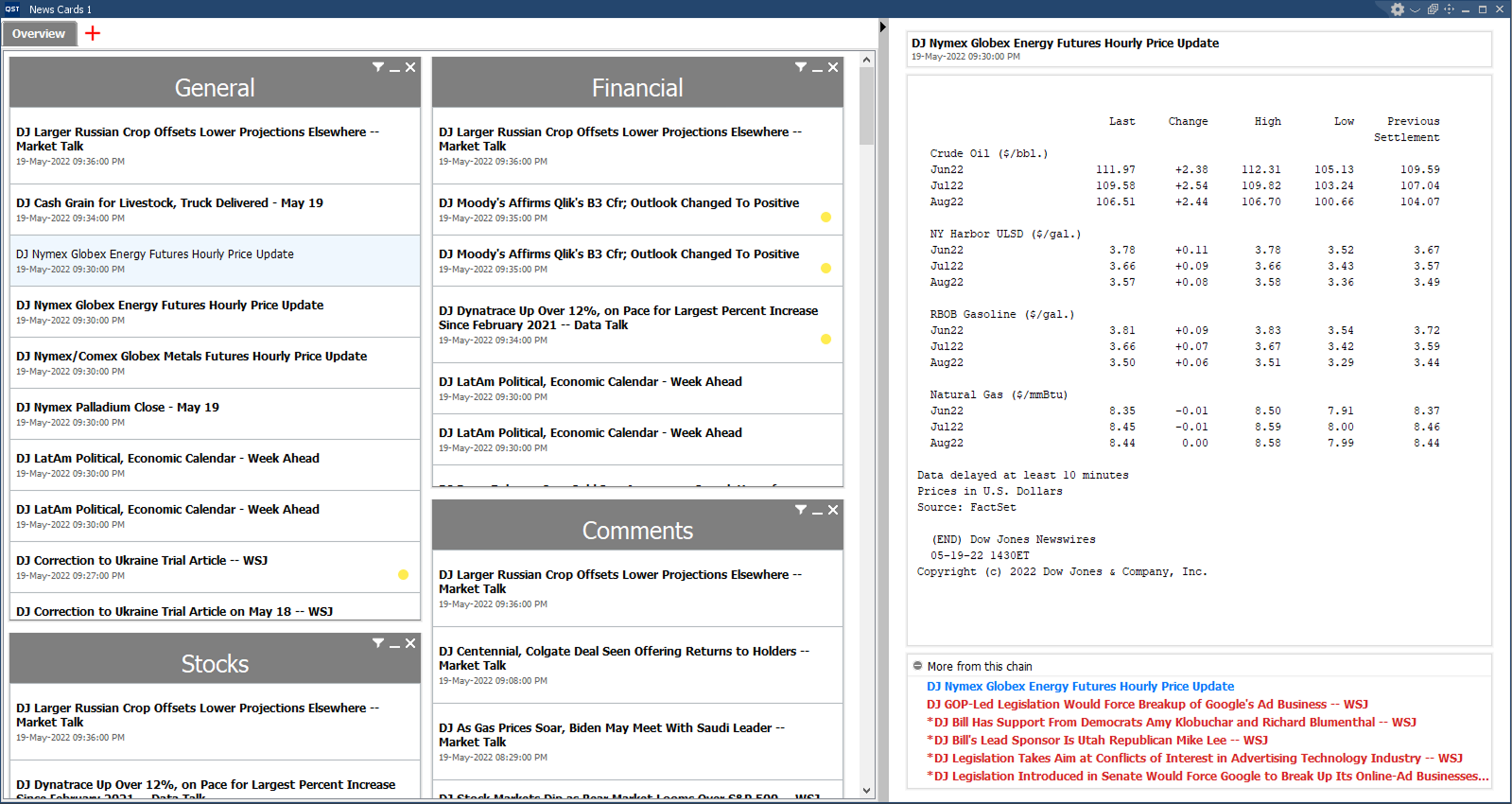

News

This dedicated module displays news from different major news providers.

News headlines are filtered by several default categories.

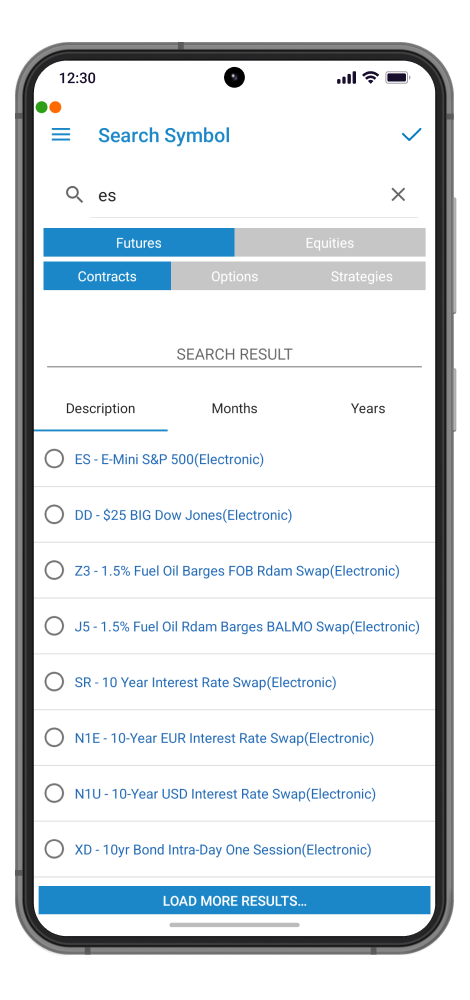

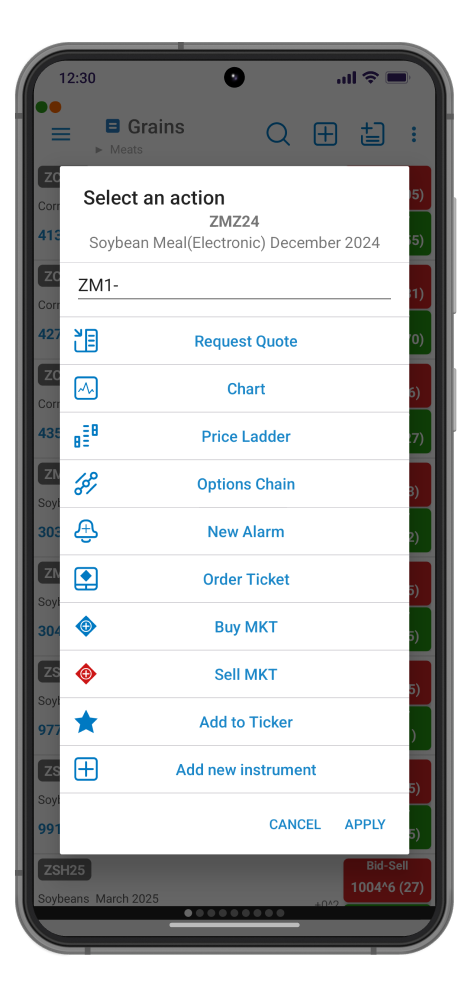

Instrument Lookup

Available all over the app whenever is needed a dedicated toll can help find any symbol no matter how complex is the final instrument.

Search can start from simple keywords, to futures, equities, options, strategies. The search controllers and information will dynamically update according to the input info in order to narrow down the search and get to the final result as fast as possible.

Extra information and details will help guide the search.

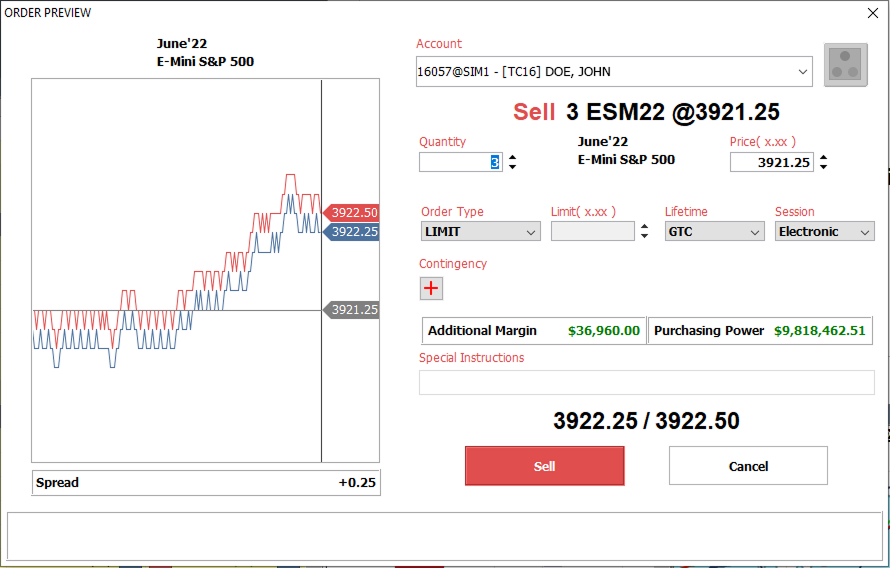

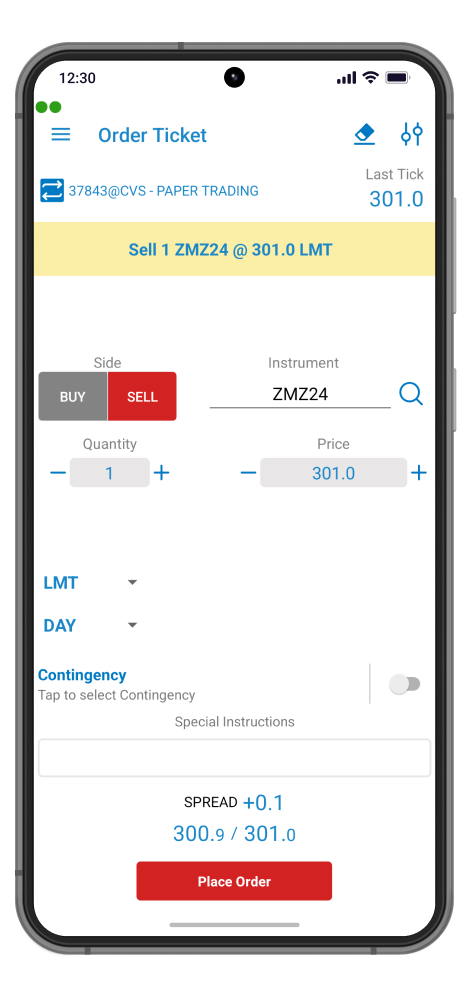

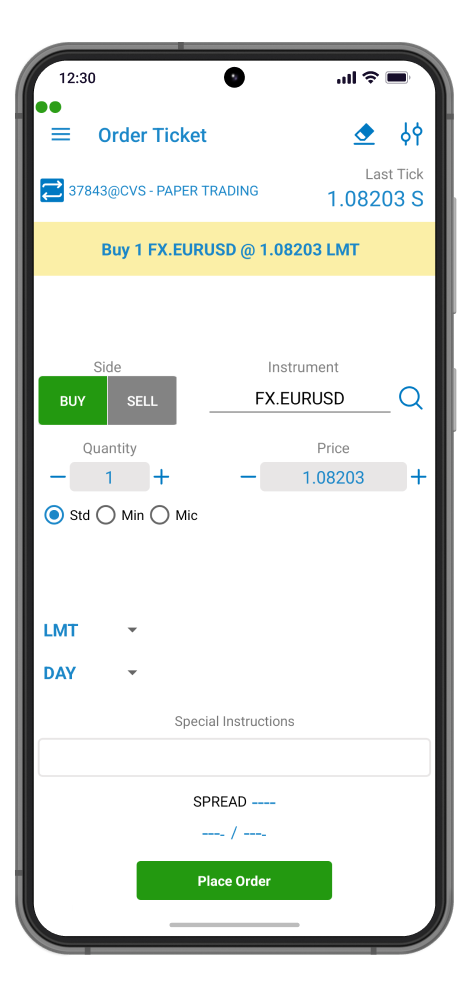

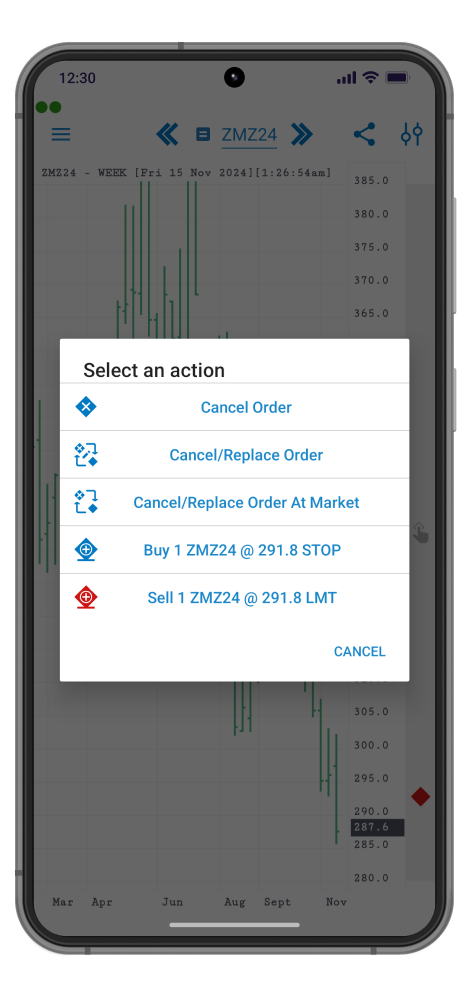

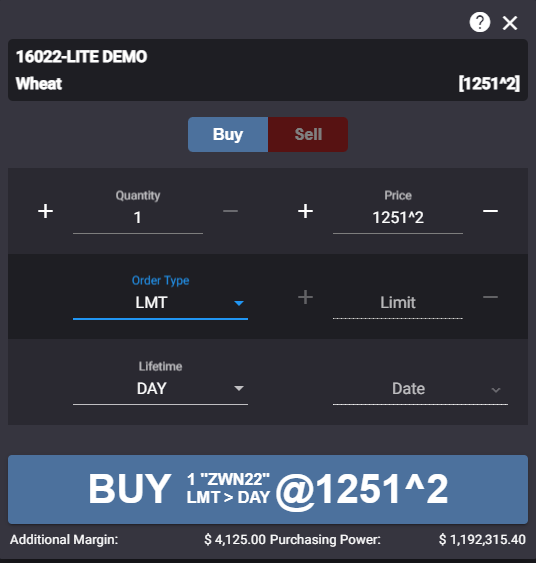

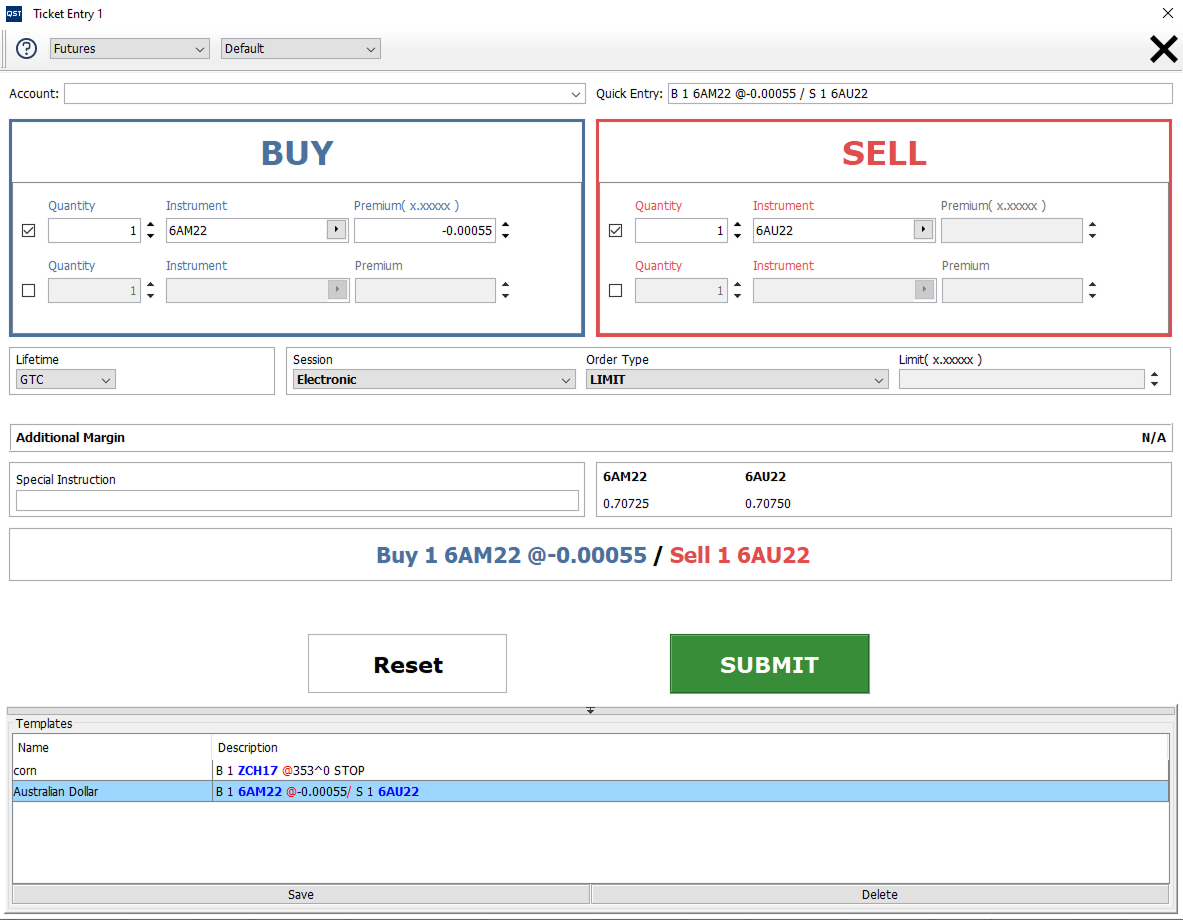

Order Entry

Spread, Bid, Ask, Last data is updating real time on screen.

Custom defined precautionary limit for quantity can be defined to be displayed in a dedicated Warning Dialog.

Dedicated preview modes for Offset and Reverse actions are available to be custom defined.

Quick navigation to favorite screens after placing an order are available:

2/2

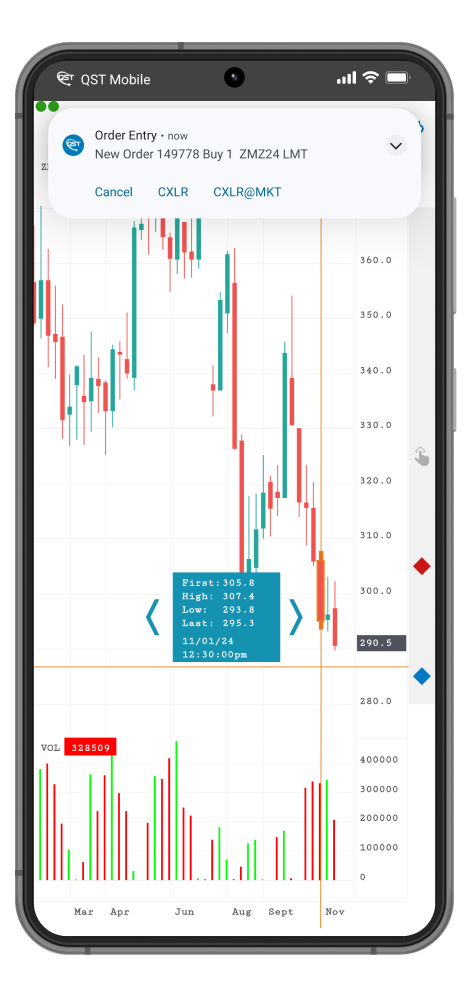

Order Entry

A dedicated screen for placing orders for all kinds of instruments is always one tap away from different screens like: Quotes Monitor, Price Ladder, Fullscreen Charts, Options Chain, Quote Details, Orders & Positions Monitor and many more.

Easy to configure different aspects of the order:

Orders placed will appear in the Orders and Positions module and order Activity Log.

Important updates of your portfolio can be shown in Push-Notifications, In-App Notifications or Alert Dialogs. All these updates come together with a wide range of dedicated Order Entry Actions for a convenient and quick interaction.

1/2

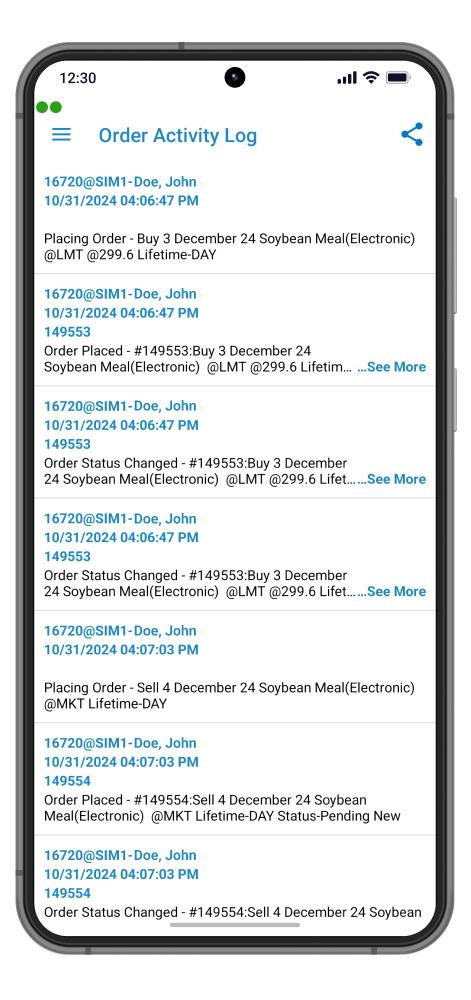

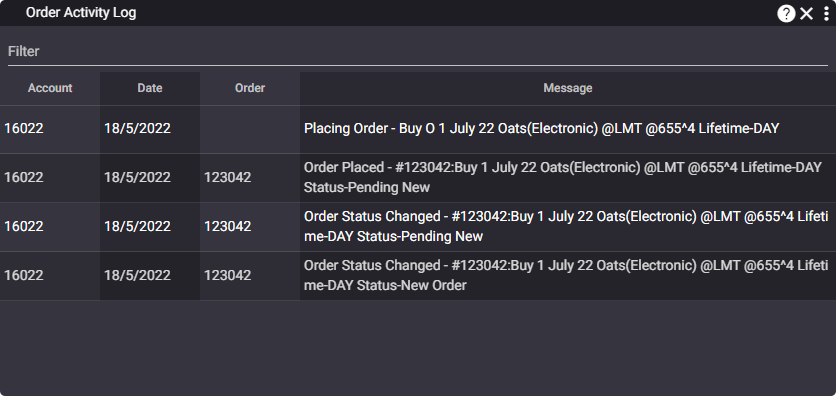

Order Activity Log

Order Activity Log, displays all the information about the orders entered during a session, including detailed data about orders such as account, status, side, quantity, instrument name, price, lifetime. Furthermore, it displays the fills, the new fills, the canceled orders.

A dedicated button for a quick & easy pdf report is available in order to keep track of your trading activity.

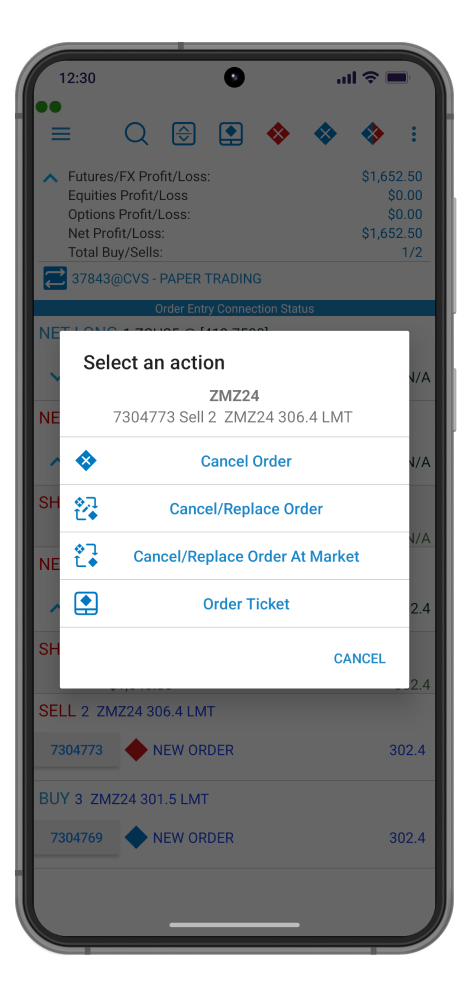

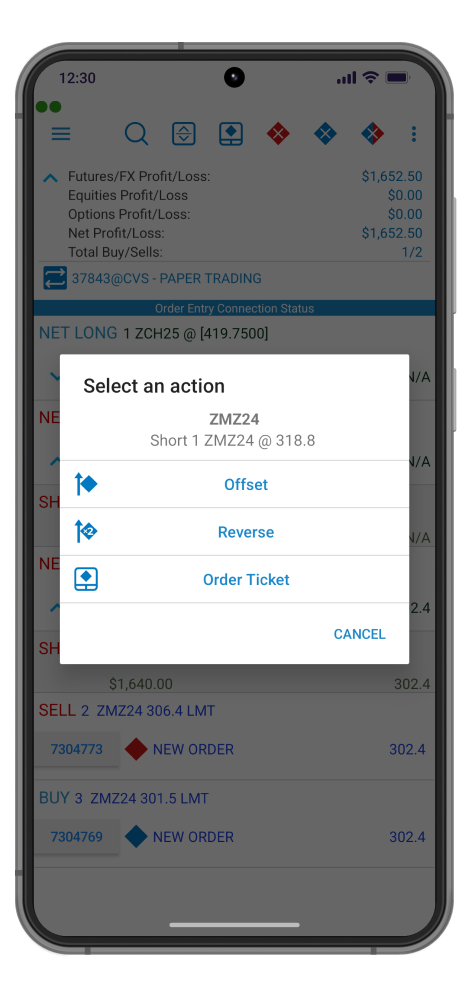

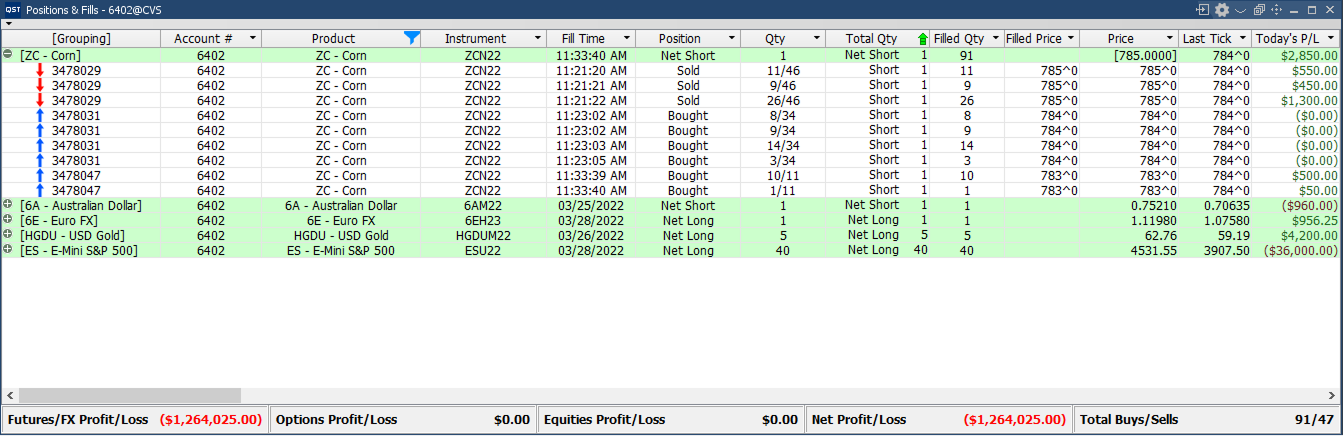

Orders & Positions

Order Entry actions:

Dedicated action buttons for: Switch Account, Order Ticket, Cancel All Sells, Cancel All Buys, Selected Currency, Export Order Entry portfolio as PDF.

One tap to enter Order / Positions Details with detailed data and dedicated trading actions.

A fullscreen portfolio can be shown due to a collapsible Profit&Loss header.

2/3

Orders & Positions

Provides a real-time summary overview on the Order Entry portfolio. Offers a large set of Order Entry specific actions for selected orders or positions.

Advanced search for a quick localization for an Order or Position based on keywords that will look into all portfolio.

Detailed information about a selected order or position.

Extra data is available at one tap away through dedicated controllers as: Order Number Button, Expand/Collapse button for Net Positions, Expand all/Collapse all Net Positions.

For a fast identification of Order and Position Type/Status, we use dedicated color codes for labels and icons.

Real-time streaming Profit&Loss updates for all portfolio are available.

1/3

Request For Quote

Place RFQ offers the possibility to place your own RFQ. This functional module is available from different screens for quick access.

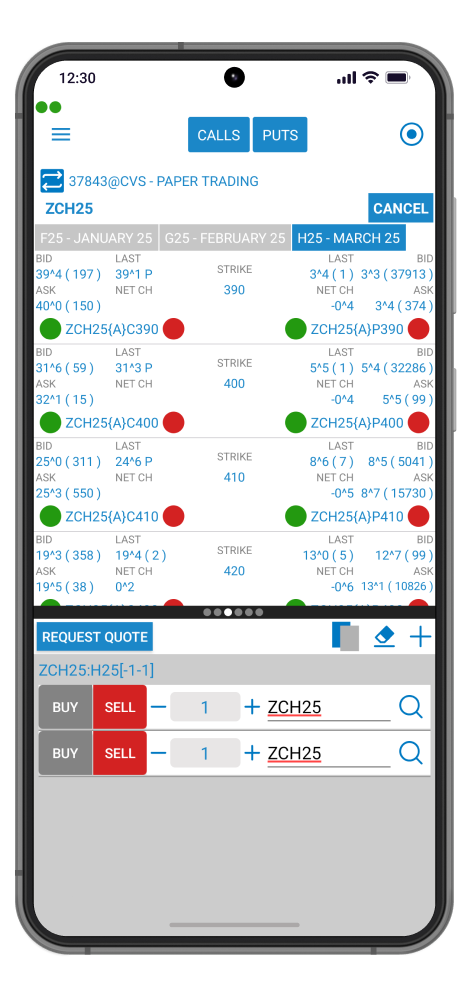

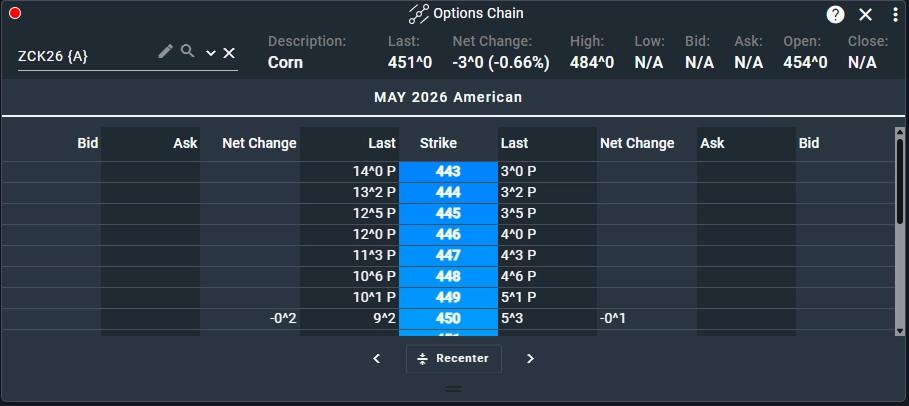

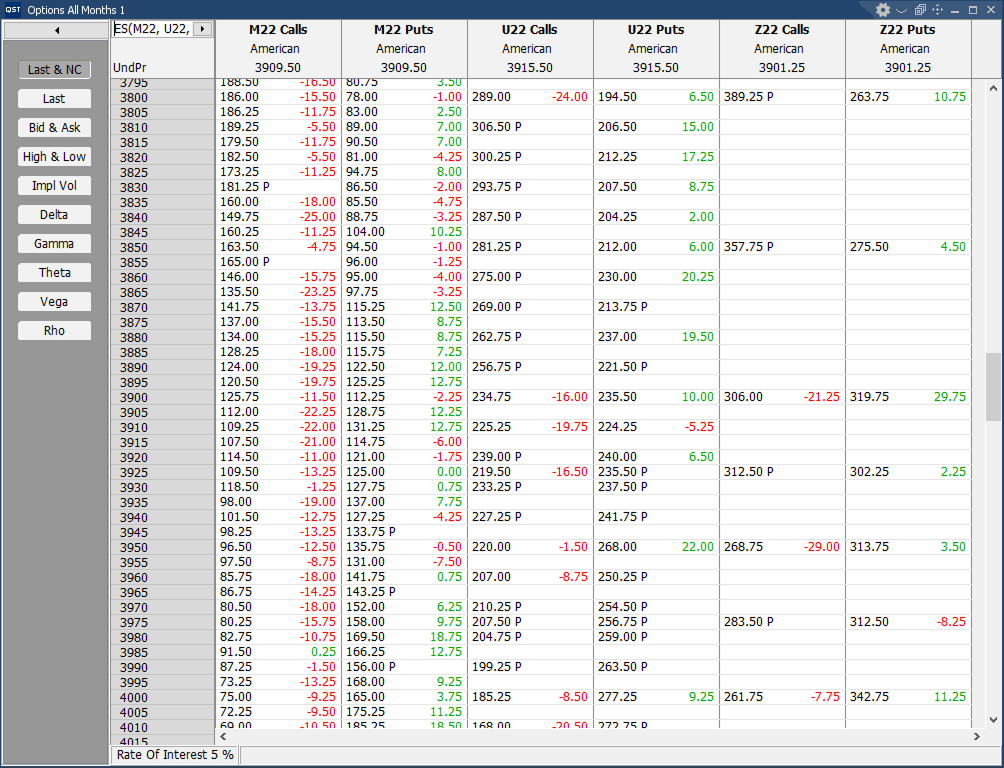

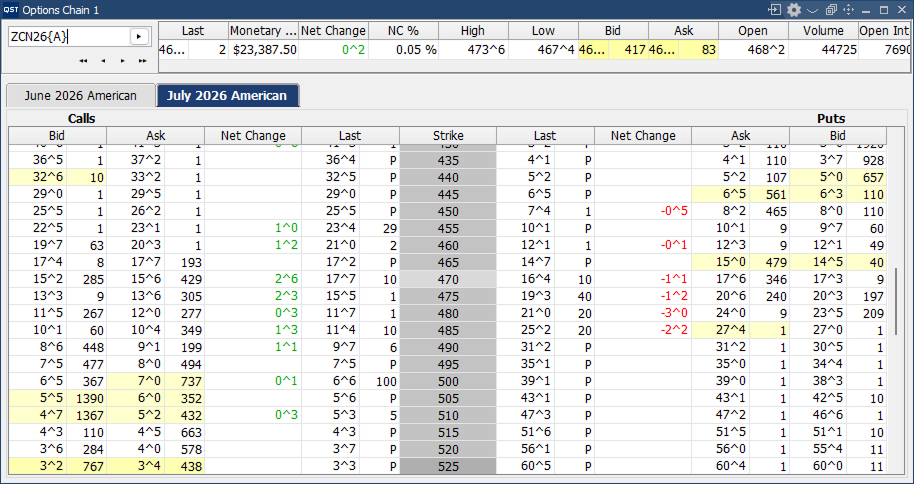

Options Chain

Options Chain can display all the options for any underlying instrument with the ability to trade individual options directly from the module.

1/2

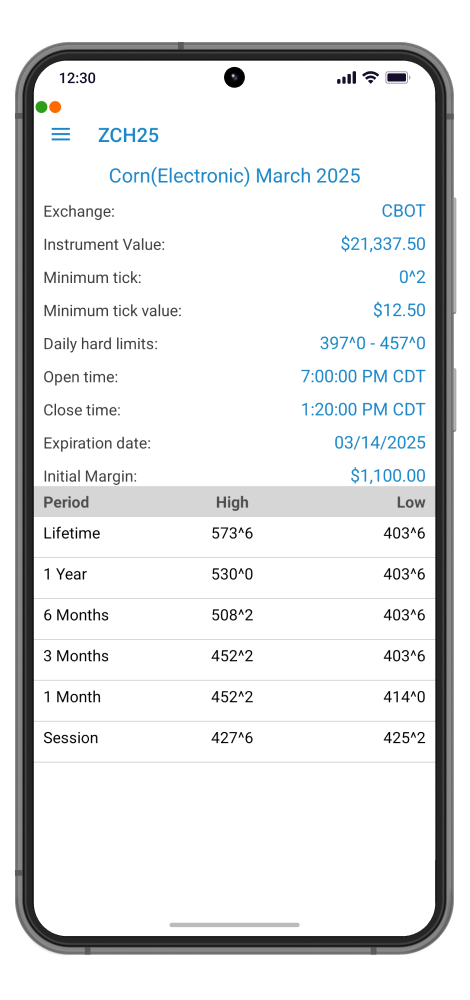

Instrument Details

Important information for any instrument is available from different modules of the app in this dedicated screen. It supports different types of instruments: futures, options, strategies, FX, CFDs and equities.

Quote Details

2/2

Quote Details

1/2

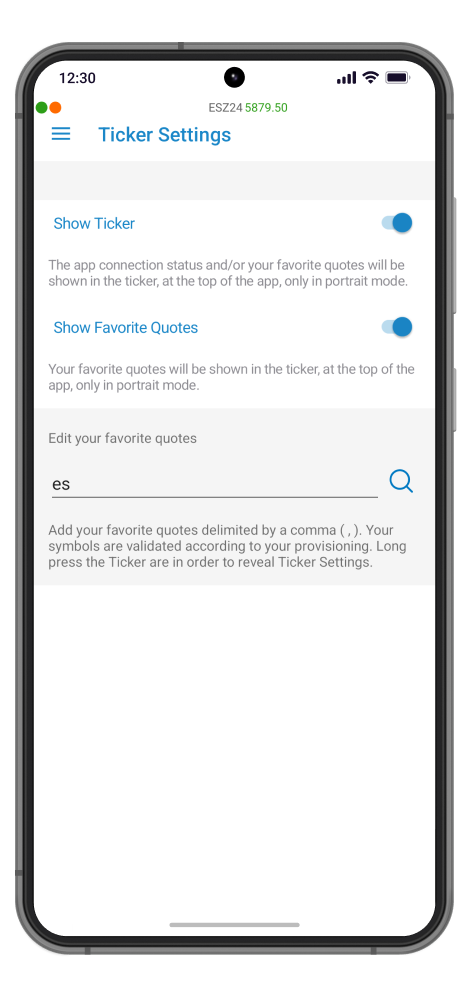

Ticker

You can monitor your favorite quotes in a Ticker view available at the top of your app. The Ticker view, once enabled, is persistent in all screens and modules.

You can edit your favorite quotes from General -> Ticker Settings -> Edit your favorite quotes. Ticker Settings view can be revealed with a long tap on the Ticker area.

1/2

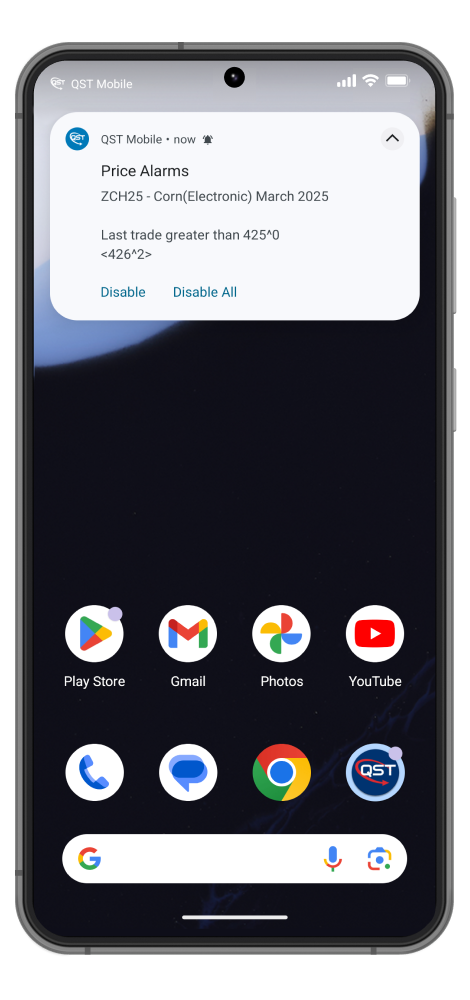

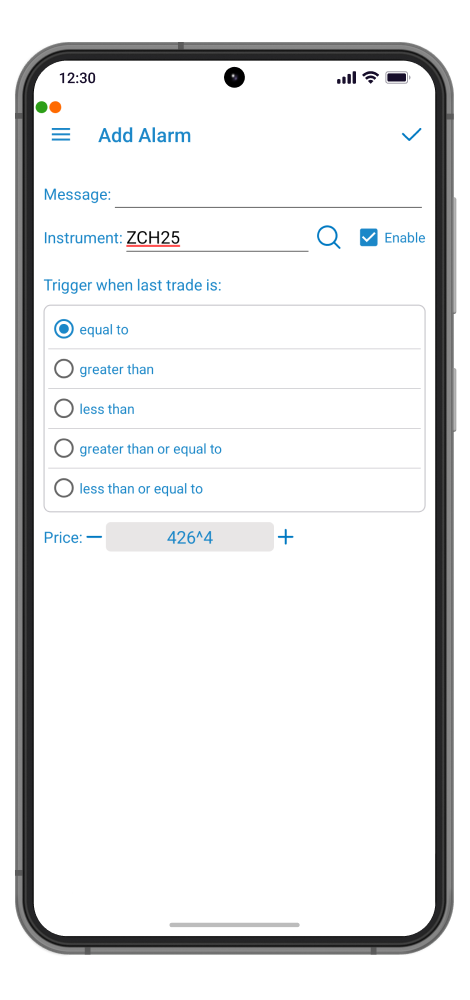

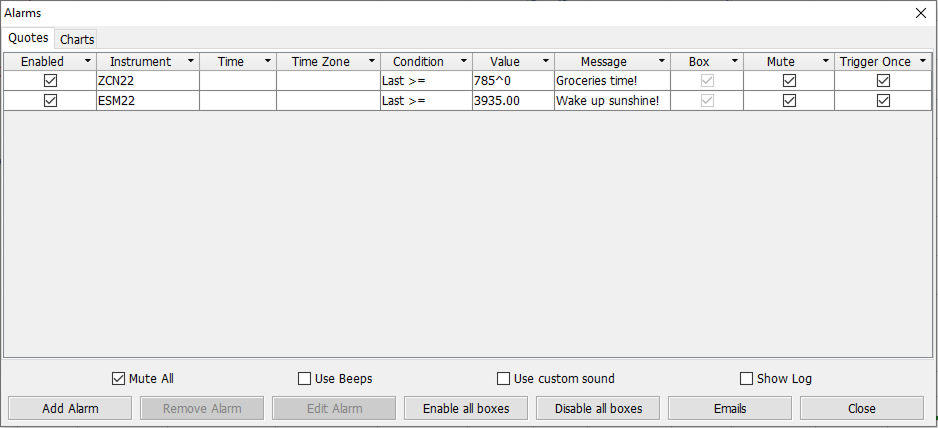

Alarms

Ready to set from different screens as: Quotes Monitor and Quote Details. Price Alarms overview can be shown in Push Notifications, In-App Notifications and Alert Dialogs. A set of default actions are available when interacting with Price Alarm’s Push and In-App Notifications.

2/2

Alarms

Price Alarms can be set on any quote with various conditions and alerting modes.

1/2

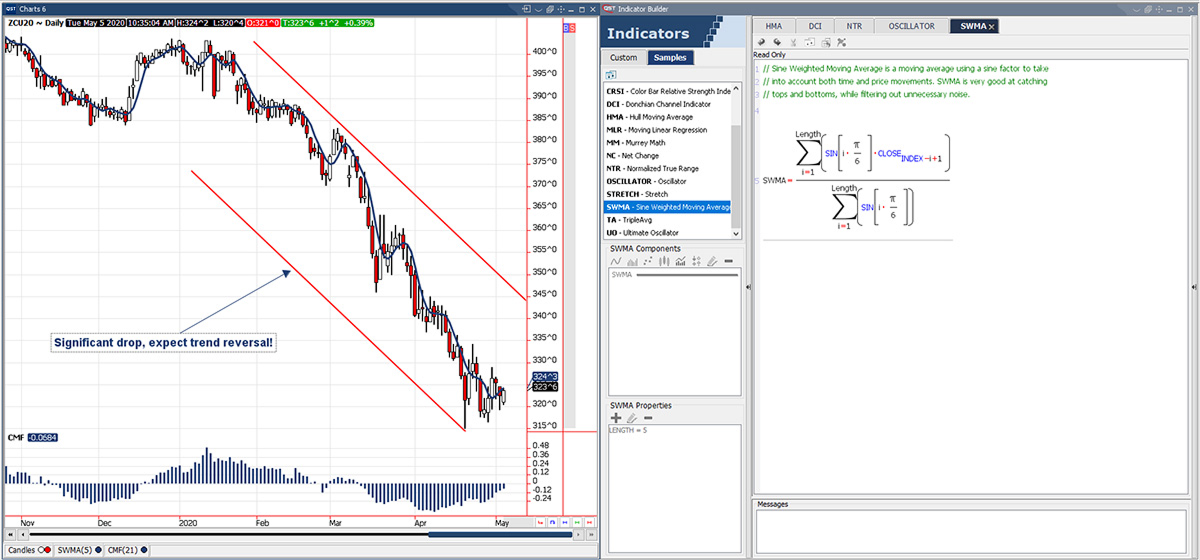

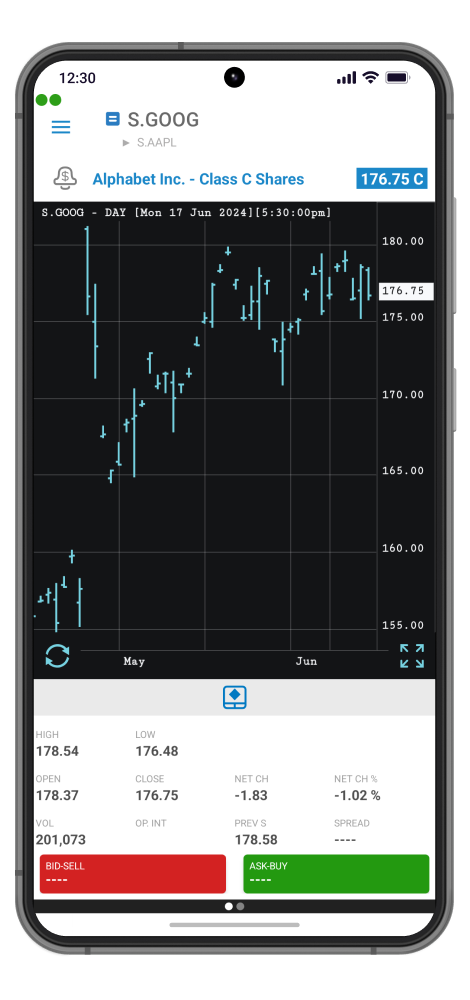

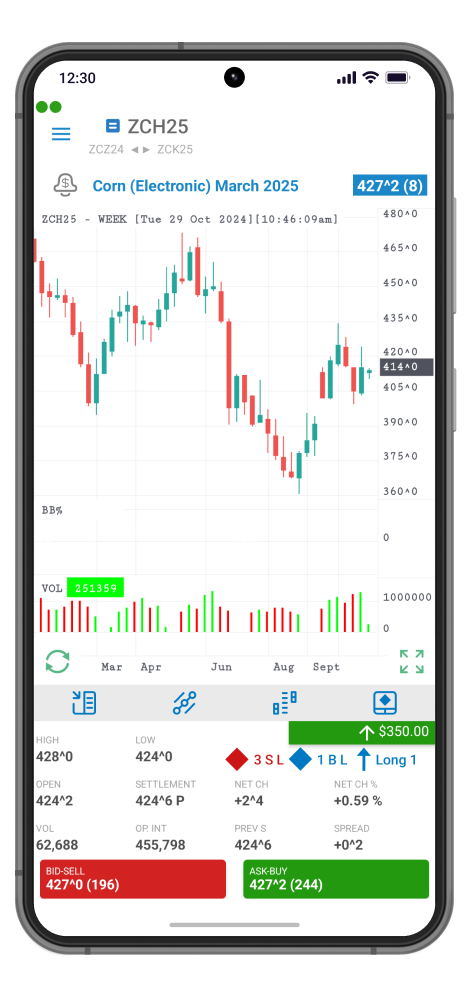

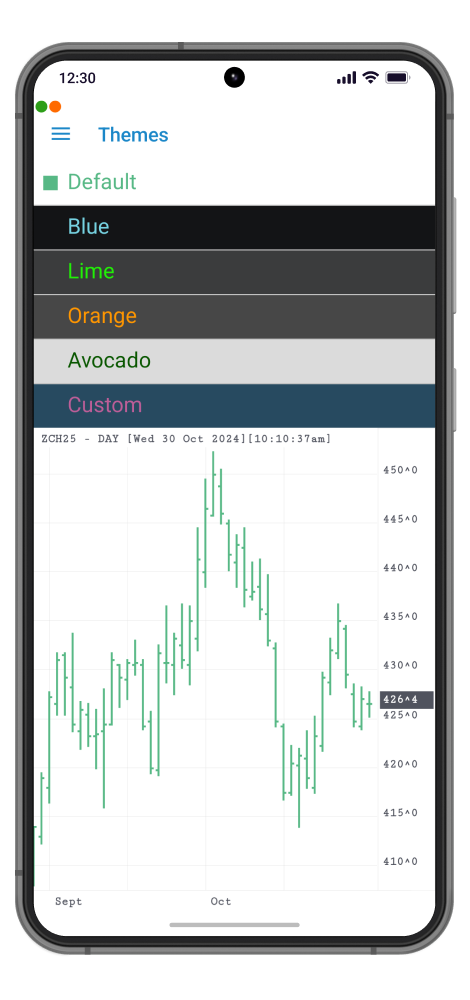

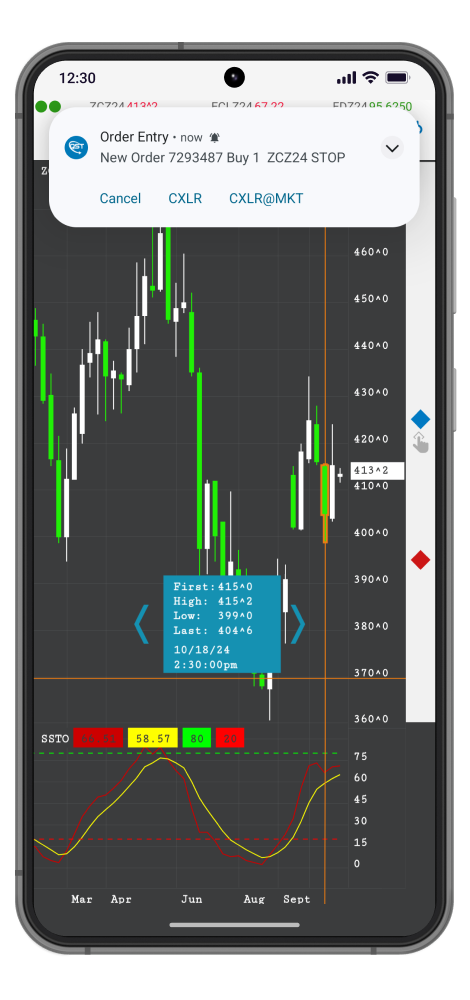

Charts

3/3

Charts

2/3

Charts

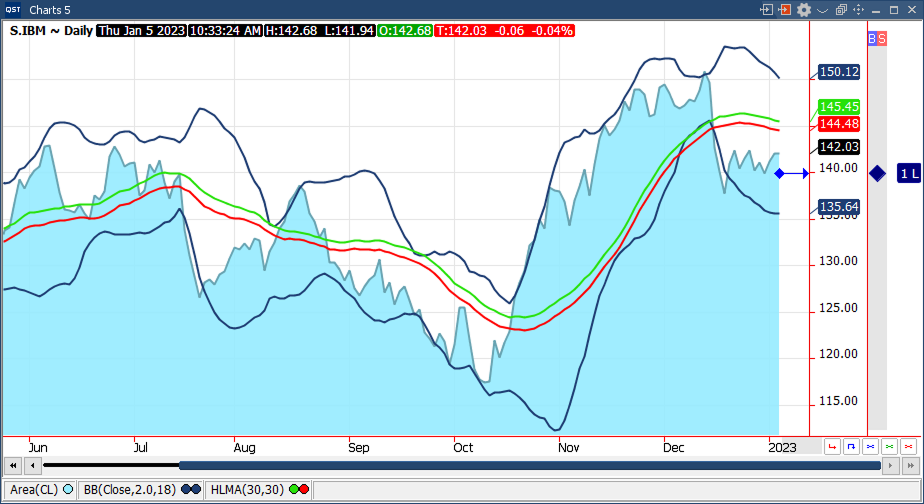

Advanced HTML5 real-time charts with a wide selection of tools, settings, and programmable indicators.

1/3

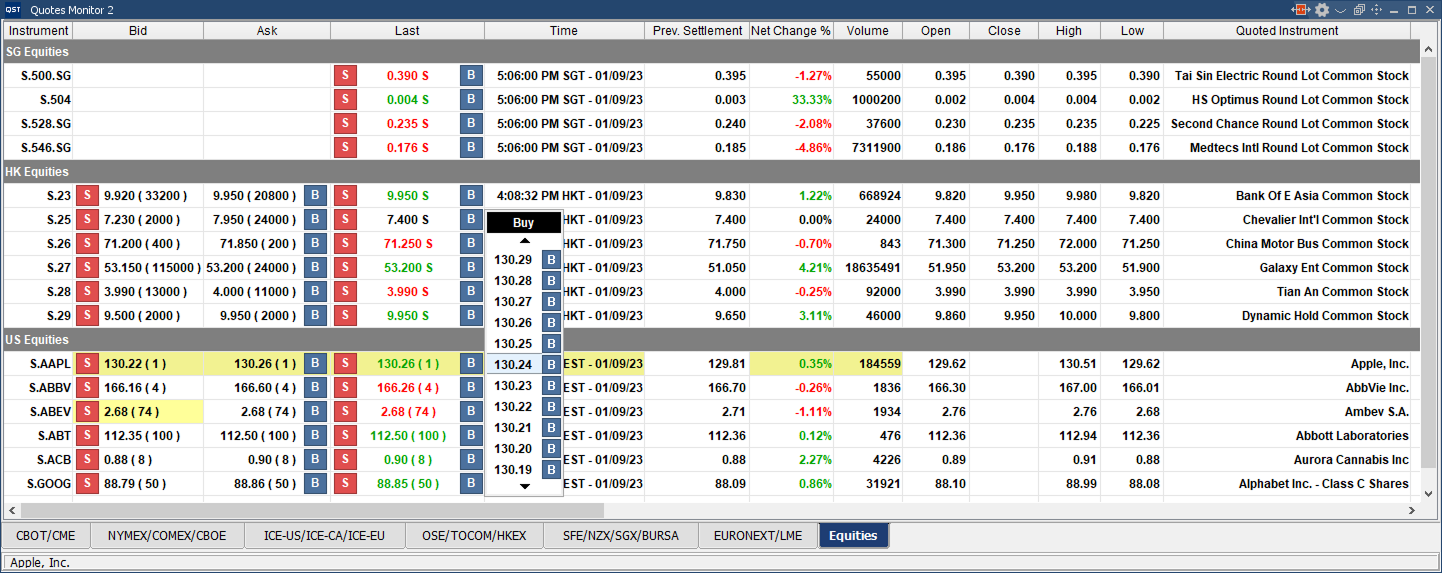

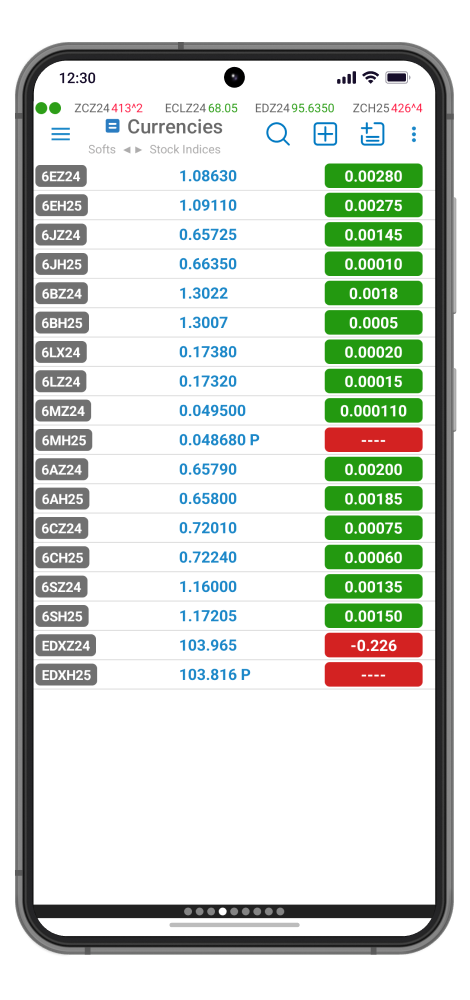

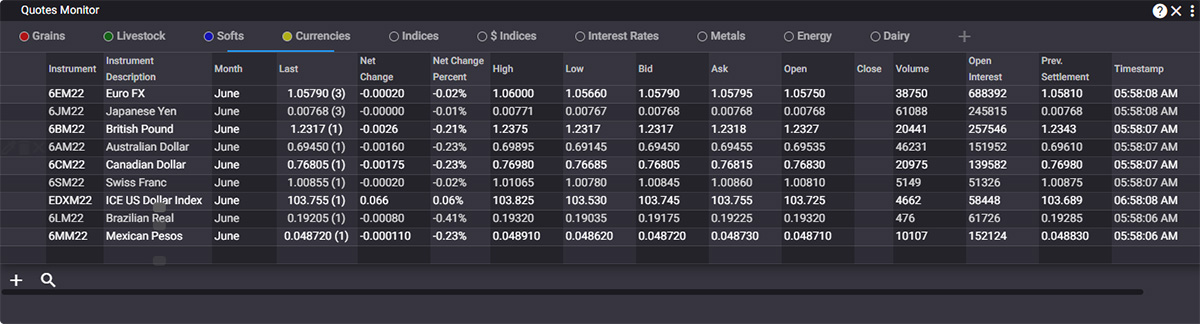

Quotes Monitor

3/3

Quotes Monitor

Customizable:

2/3

Quotes Monitor

Quotes Monitor offers a highly customizable quote montage that provides detailed quote information organized into multiple pages with user-defined titles. Intuitive user interface, customizable pages and in detail quote layout. Quick and easy switch actions between pages and instruments.

1/3

Overview

A persistent Ticker View at the top of your screen with your favorite quotes, updated continuously throughout the trading session.

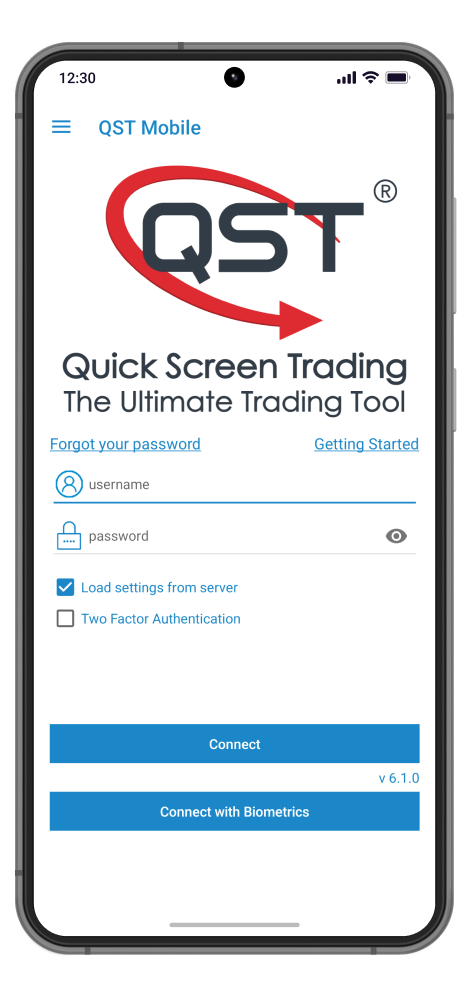

Two Factor Authentication and Biometrics provide both enhanced security and an easier login experience.

3/3

Overview

Real-time streaming quotes with customizable layout. Highly reliable and accurate data.

Internet-based mobility for anytime/anywhere access.

The best combination of sophistication, usability, performance and price.

One tap trading operations available from all of our main modules: Quotes Monitor, Price Ladder, Full Screen Charts, Options Chain, Orders & Positions.

2/3

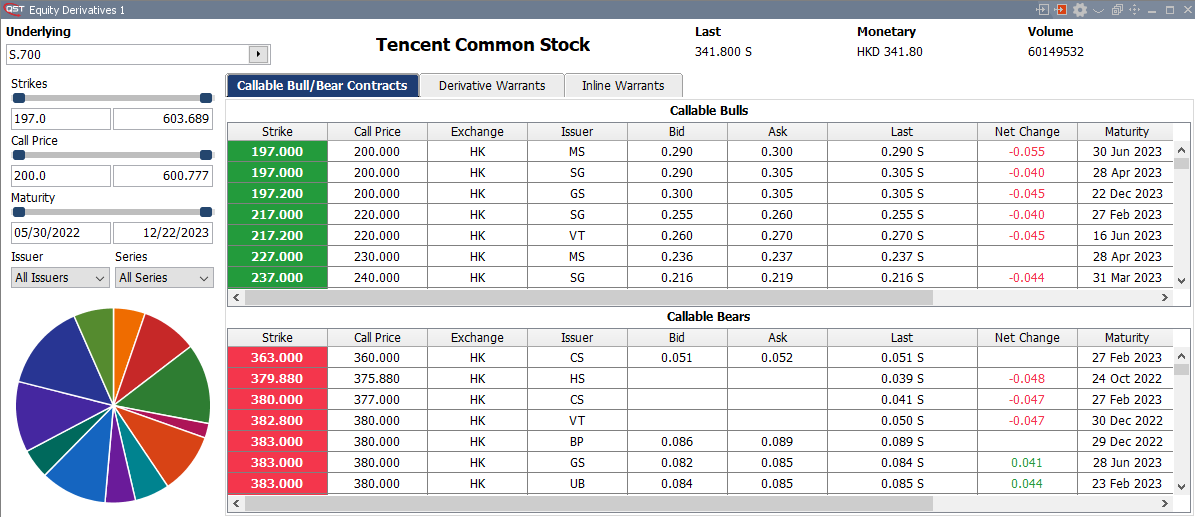

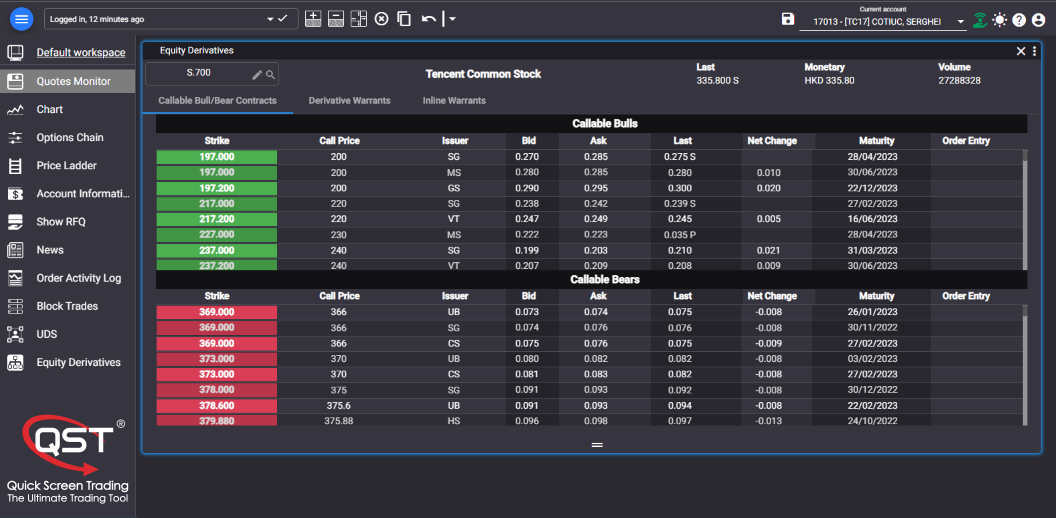

Equity Derivatives

Shows all the derivatives grouped by type for a given underlying.

Shows all the derivatives grouped by type for a given underlying.

E-px

Overview

QST Mobile is a revolutionary futures, equities, FX, and CFD trading application that combines comprehensive, fast and flexible order entry/order management with world-class charting and analytics, real-time quotes, and news.

QST Mobile is available on iOS and Android platforms, with matching functionality and full native user interface, complying with the latest Google and Apple User Interface Guidelines.

Fresh updates are available on Google Play and App Store, bringing new features backed up by a 24/6 customer support service.

1/3

Charts

Advanced HTML5 charts with a wide selection of tools, settings, and programmable indicators.

Block Trades

Filterable streaming list of block-trades listed by different exchanges. All in one place.

Order Activity Log

Equity Derivatives

Equity Derivatives module supporting:

Account Information

Shows the balance for the current account.

Real-time account calculations including:

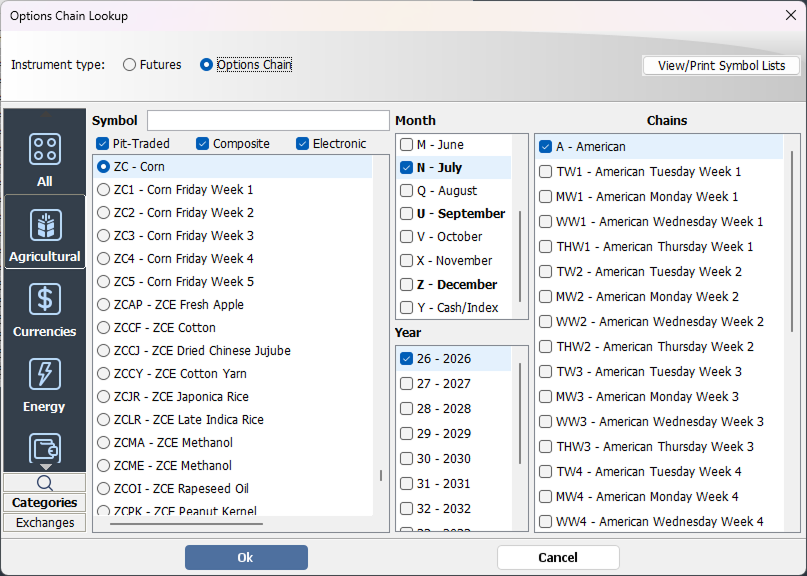

Options Chains

View available options for a certain futures contract.

Customizable:

Price Ladder

News

Customizable:

Quotes Monitor

Customizable:

Orders & Positions

Order Entry

Place orders from Charts, Quotes Monitor, Options Chain, and Price Ladder.

Overview

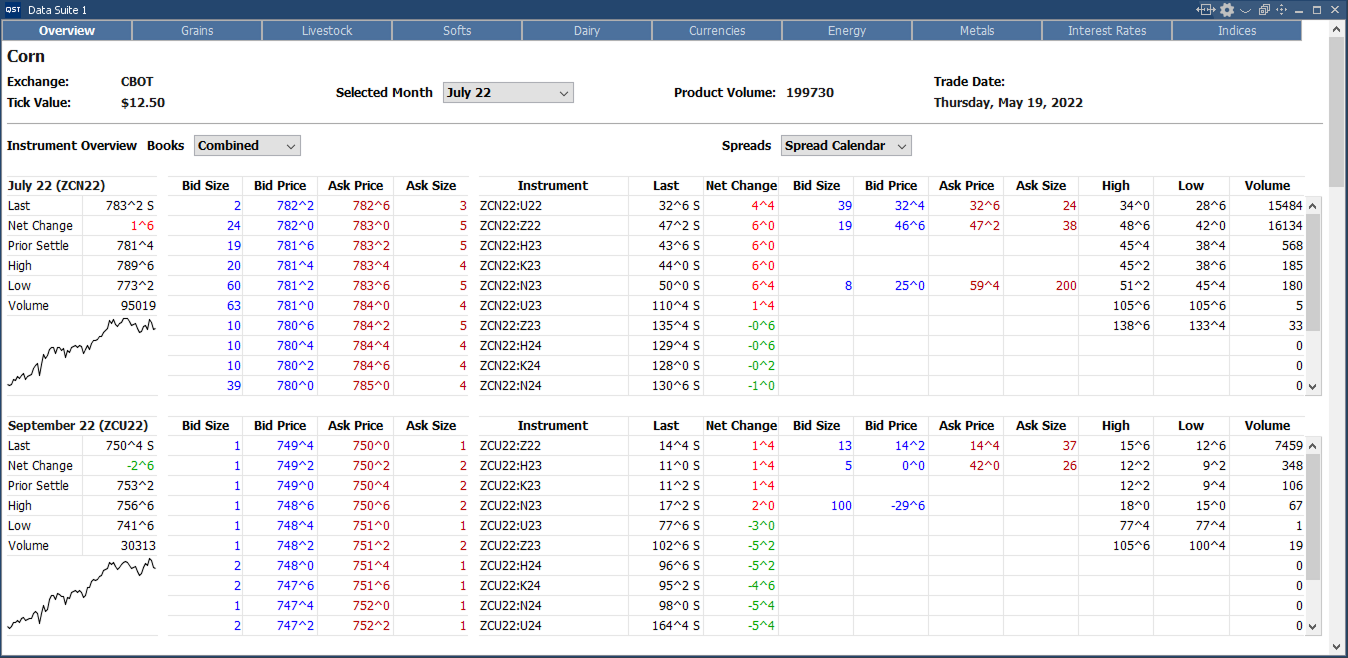

Spread Matrix

Trading & Analysis Features

Customization & Navigation

Data Suite

Block Trades

Account Information and Summary

Margin Requirements

1/2

Alarms

Instrument Lookup

Scrolling Ticker

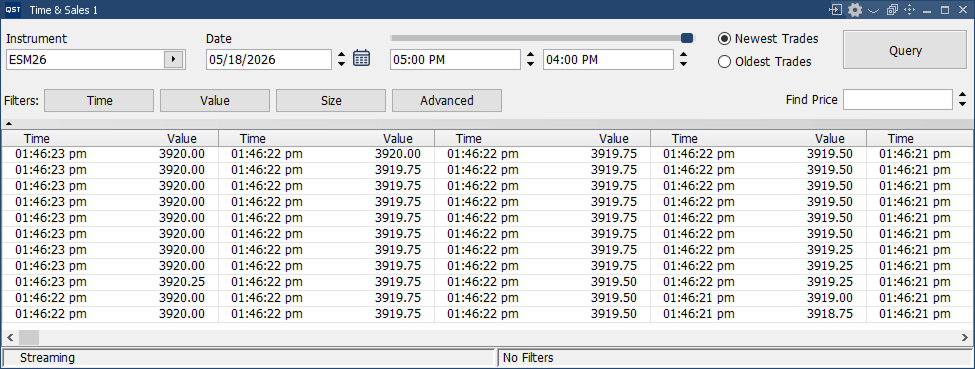

Time & Sales

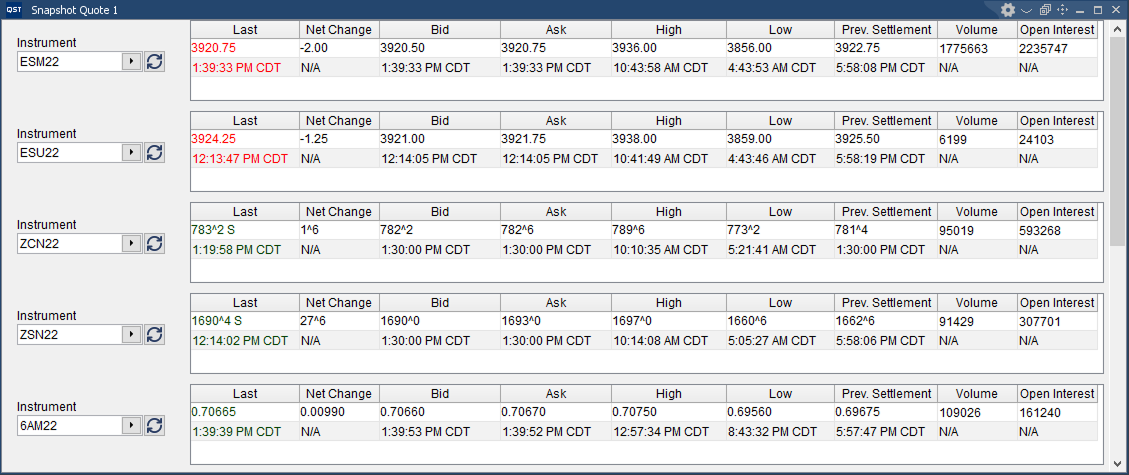

Snapshot Quote

Customization Features

Integrated Market Tools

Real-Time News

Options All Month

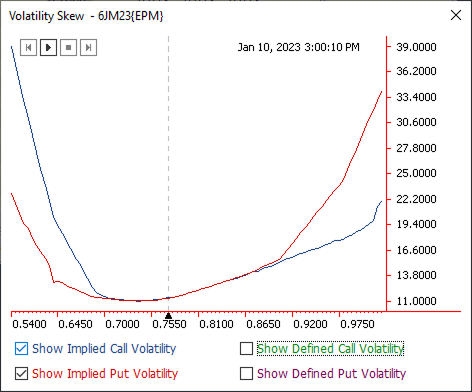

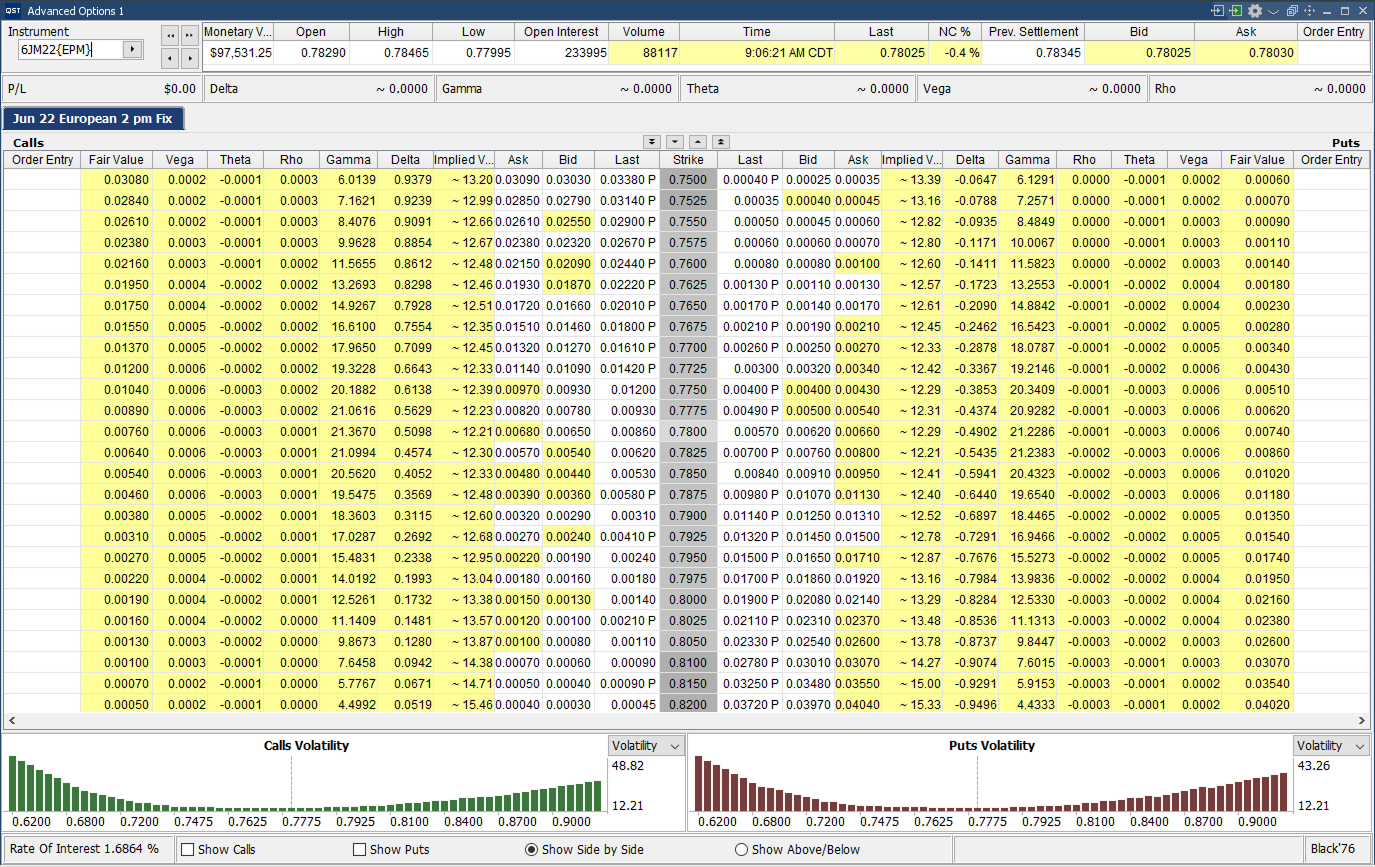

Advanced Options Analytics

Trading Features

Advanced Options

Integrated Strategy Builder for creating and managing advanced options strategies.

2/2

Options Chain

Customization Features

Trading & Analysis Features

Depth Of Market

Customization Features

1/2

Price Ladder

1/3

Order Entry/Management

1/2

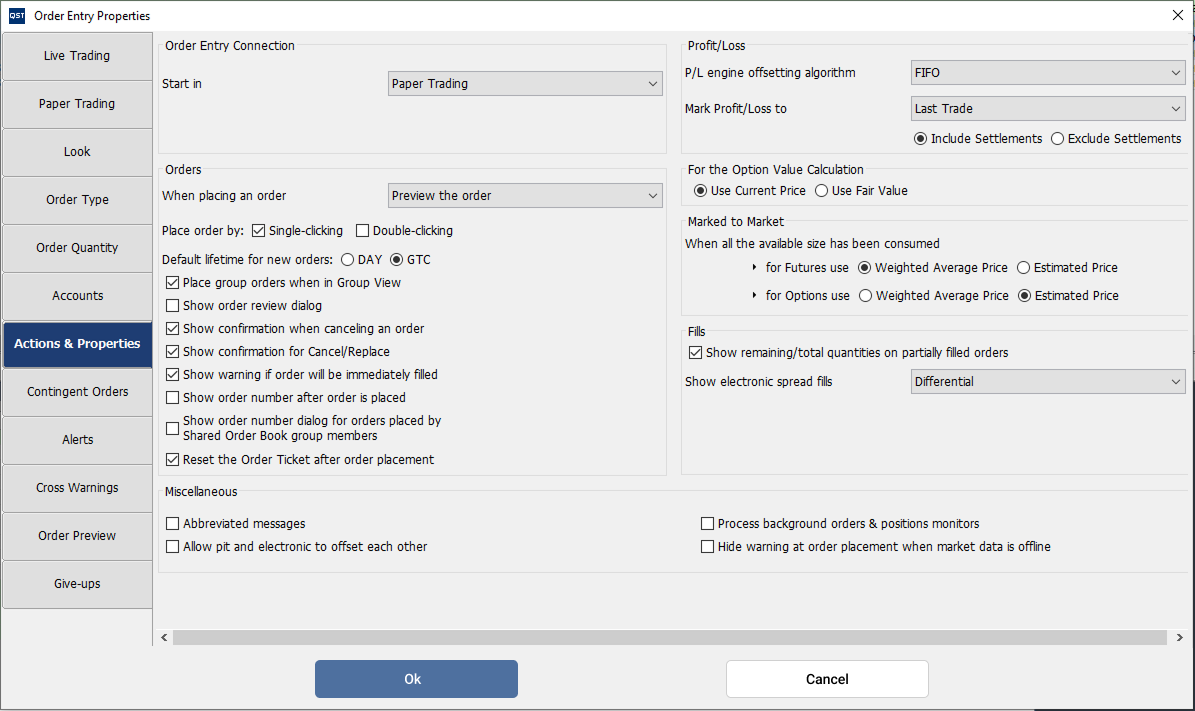

Order Entry Properties

Customizable Order Behavior

1/2

Orders & Positions Monitor

Advanced Filtering Capabilities

1/2

Quote Board

Customization Features

Integrated Trading & Analysis Tools

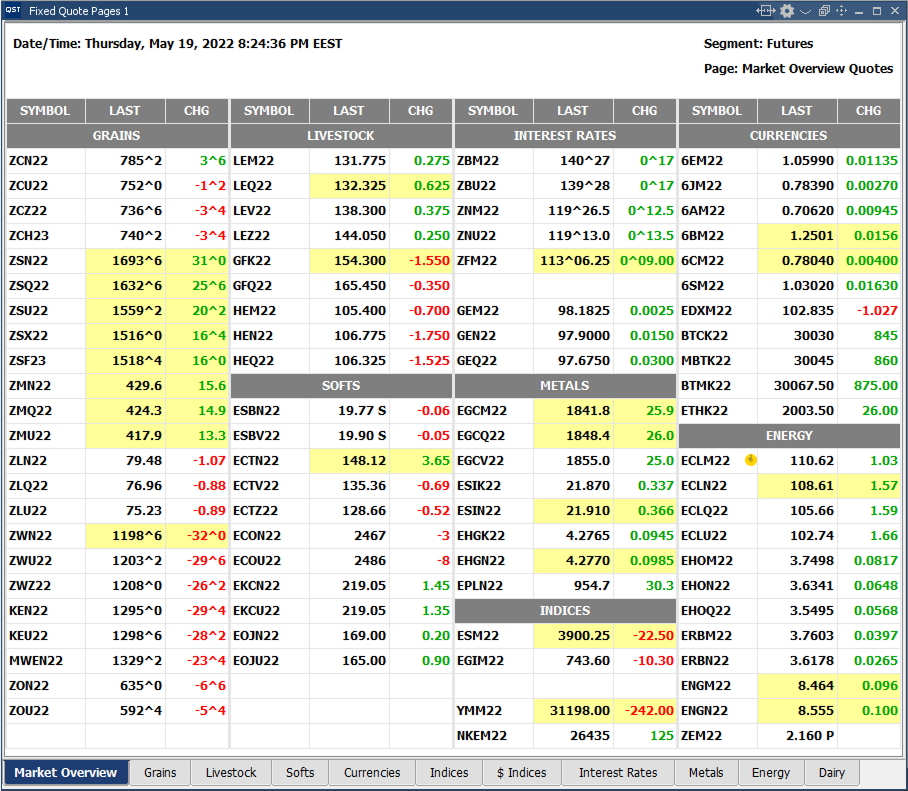

Fixed Quote Pages

Quotes Monitor

1/2

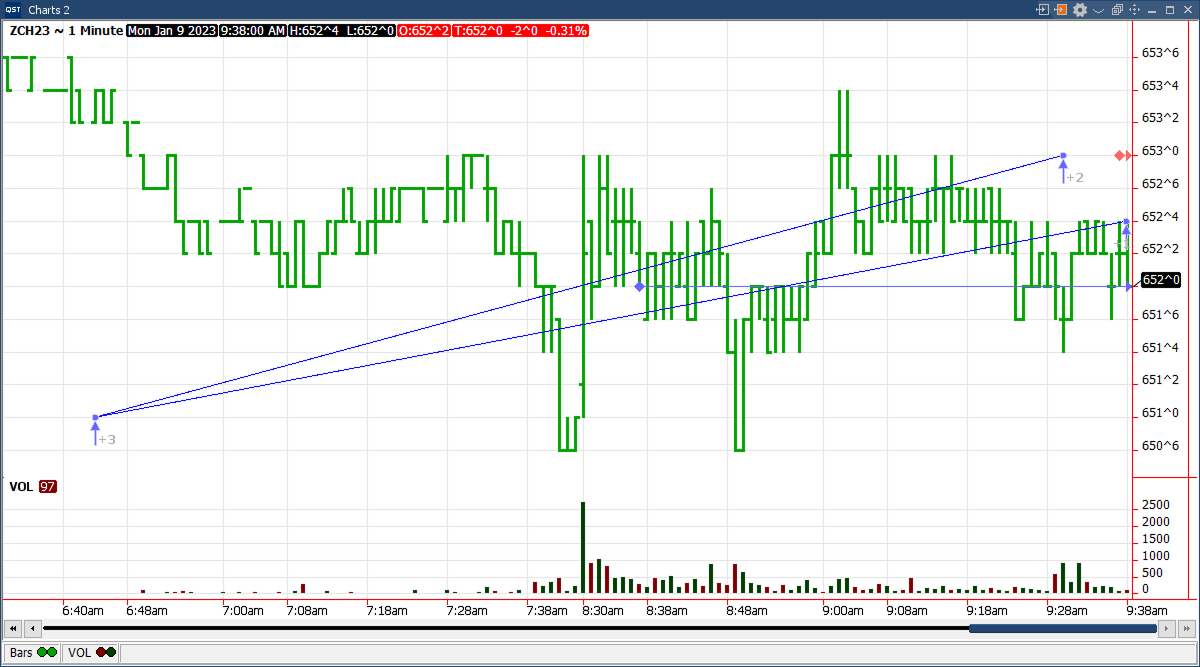

Charts

3/4

Charts

2/4

Charts

1/4

Overview

3/3

Overview

2/3

Overview

1/3